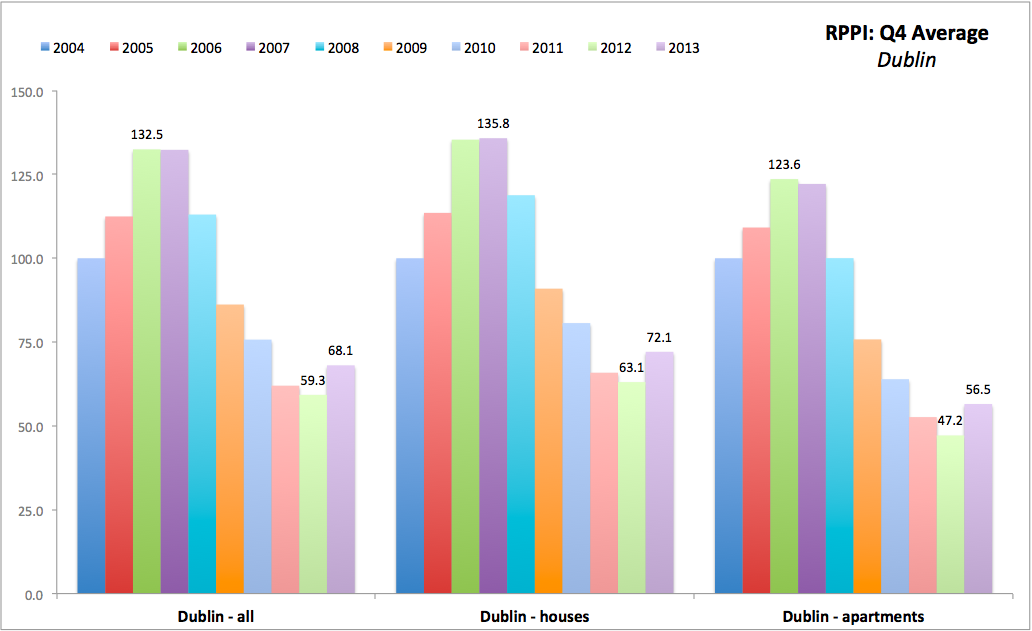

AN interesting article on Norway's petrodollars 'curse of oil' economy's future from Reuters, headlined "End of oil boom threatens Norway's welfare model" (see: http://www.reuters.com/article/2014/05/08/us-norway-economy-insight-idUSBREA4703Z20140508)

This begs a question - are things really going South for Norway?

Sure, the country has basically nothing to show for its oil bonanza in terms of indigenous industries development or investment. Sure, it is giving cash left-right-and-centre to various social entrepreneurs, native enterprises, cultural ventures etc which produce virtually nothing of any demand outside Norway and questionably fulfil real demand inside Norway.

But, really, are things getting visibly bad on the horizon? And are they getting worse than in other Nordic countries?

Here are some charts summarising economic and fiscal performance of Norway compared to the rest of Nordics and Sweden.

Starting with General Government Revenue as % of GDP:

The above shows couple of things:

- Norway's revenues are comfortably above those for Sweden and for Nordics. Which is the same as to say that Norway's economy is more heavily dependent on Government sector. This, of course, includes gas and oil revenues.

- But the share is has been rising between 1994 and 2008 not only because revenues from North Sea are rising, but also because rest of economy activity was getting trapped in state-dependency.

- Crucially, the revenues have been on downward trajectory since 2009 and this is forecast to continue into 2019. Pressure is mounting.

- The opposite to Norway's trajectory is happening in the rest of the Nordics and Sweden. In particular, following massive Swedish and Finnish crises on the early 1990s, share of Government in the economies of the Nordics ex-Norway has fallen steadily from 1988-1991 peak toward the trough around 2010 in the Nordics and still heading down for Sweden.

All in, Norway is showing signs of serious strain on revenue side, but it is not in a crisis… not yet.

What about the Government Expenditure?

The above shows the following:

- Basic expenditure side of the fiscal equation is still better in Norway than in the Nordics and Sweden.

- However, out on 2019 range forecasts, Norway is starting to actively catching up with Sweden and converging toward the Nordics.

Again, not a crisis yet… but dynamics are not encouraging.

On Government Debt front, Norway is doing well, especially compared to the Nordics:

And it still outperforms the Nordics on Current Account side:

- One caveat here is that Norway's current account surpluses are solely down to oil and gas revenues. The country does not deliver value for money in any other sector, including, increasingly in its aqua-farming sector. Meanwhile, Sweden generates current account surplus ex-energy and raw materials.

On balance, there is a serious problem emerging for Norway: current account surpluses are on downward trajectory since 2006, and decline is forecast to accelerate. Good news for Norway: there is no deficit in sight. Bad news: in order to achieve quick transition of its economy away from oil & gas dependency, it will need massive investments and capital imports - which can force the current account balance into deficit very quickly.

The problem of fast rising public spending against revenues and declining public surpluses is often best can be seen in level terms, in current spending, instead of as a share of GDP. Here is the summary chart:

As noted earlier, this shows:

- Rapidly rising state spending, for not rather well matched by revenues.

- Rate of revenues increases declining from 2012 on and being outstripped by projections for expenditure increases for 2013-2019 period. These are mostly down to forecasts, so not materialised yet… but still - a warning shot.

- Exchequer surpluses declining from local peak in 2012.

- On positive side, surpluses are still present in forecast out to 2019, which is a strong position to have.

Here is a net summary on various growth rates over decades averages:

and a chart showing the gap between Sweden's GDP growth rate and public spending rate, and that for Norway:

Key takeaways: Norway is not yet flashing red, but its growth in public spending is not sustainable in the environment of falling net revenues from energy sector. Structural weakness in the Norwegian economy is basic lack of real economic growth outside the energy sector, compensated for by the over-reliance on public spending and investment.

{kind=link}