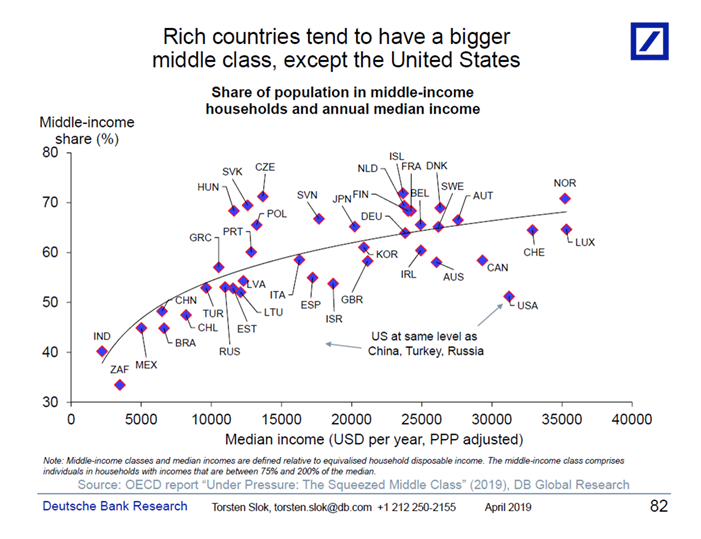

An interesting and insightful 2016 paper from John Komlos of CESIfo, titled "Growth of Income and Welfare in the U.S. 1979-2011" (CESifo Working Paper No. 5880), paints the pretty dire picture of the post-1980s dynamics in the U.S. labor markets, that laid the foundations of the current acceleration and deepening of political populism and opportunism not only in the U.S., but also in Western Europe.

Kolmos estimated growth rates in real incomes in the U.S. from the Congressional Budget Office’s (CBO) post-tax, post-transfer data. Kolmos also adjusts the real income data to improve the accuracy of the measures. The result is striking: "... the major consistent findings include what in the colloquial is referred to as the “hollowing out” of the middle class. According to these estimates, the income of the middle class 2nd and 3rd quintiles increased at a rate of between 0.1% and 0.7% per annum, i.e., barely distinguishable from zero. Even that meager rate was achieved only through substantial transfer payments." Of course, given that we have experienced positive growth in the aggregate economy in excess of these figures and well above the demographic change, this "hollowing out" of the middle class had to be accompanied by the "fattening up" of some other income classes, either the rich or the poor or both. Per Kolmos, it was the former one: "the income of the top 1% grew at an astronomical rate of between 3.4% and 3.9% per annum during the 32-year period, reaching an average annual value of $918,000, up from $281,000 in 1979 (in 2011 dollars)." Predictably, "...the post-tax, post-transfer income of the 1% relative to the 1st quintile increased from a factor of 21 in 1979 to a factor of 51 in 2011."

But what about the poor? Again, per Kolmos, "...income of no other group increased substantially relative to that of the lowest quintile. Oddly, the income of even those in the 96-99 percentiles increased only from a multiple of 8.1 to a multiple of 11.3."

Kolmos id this exercise for 'high' and 'low' ranges of income (depending on specific assumptions that were less and more conservative ratline to the CBO's raw data.

The results of the two calculations are shown in the chart below

Source: Kolmos (2016: 14)

In simple terms, this chart shows two interesting things:

1) The dramatic growth differential between income estimates for all quintiles compared to the top quintile is fully accounted for by the massive growth in income of the top 5% of the populations and especially by the growth in income of the top 1%.

2) The gap between high and low estimates for income growth are massive for the second and third quintiles (the middle class), and are relatively comparable for the first (low income earners) and 4th quintile (upper middle class). The gap becomes much smaller for the 5th quintile (high earners) and turns negligible for top 1%.

Kolmos attempts to convert income into more meaningful 9albeit harder to pin down) measure of well-being. To do this, he estimates the logarithmic utility function for the quintiles (logarithmic utility function preserves the property of the diminishing marginal utility - the idea that as our incomes continue to increase, each percent increase in our income results in progressively smaller gains in satisfaction/utility). Here is what he finds: "A logarithmic utility function yields a growth in welfare for the middle class of roughly 0.01% to 0.07% per annum, which is indistinguishable from zero. With interdependent utility functions only the welfare of the 5th quintile experienced meaningful growth while those of the first four quintiles tend to be either negligible or even negative." Chart below shows these estimates.

Source: Kolmos (2016: 15)

Focusing on the Percentiles section, markers 6-9 disaggregate the last 5th quintile into the ranges of top 81-90%, 91-95%, 96-99% and top 1%. It is quite evident that only top 5% (segments 8 and 9) experienced welfare gains of more than the 4th quantile cohorts.

This strongly implies that, contrary to some left-leaning policymakers' proposals and preferences, the problem of 'hollowing out' of the American middle class is not driven by the incomes of the top 81-90th percentiles, nor even by those in 91st-95th percentiles. The real source of the problem starts somewhere within the 96-99th percentile and most certainly extends to the top 1%.

The same is confirmed by looking at each cohort income relative to that of the top quintile, shown in the chart below

Source: Kolmos (2016:27)

In summary, thus, the problem with the 'hollowing out' of the middle class is not within theta 20% earners, nor within the top 10% earners. It starts much higher than that.

{kind=link}