Latest mortgages arrears data from the CB of Ireland came in with a slight surprise that most of the media should have anticipated. During the launch of the annual report, the CBofI has pre-leaked some of the top-level figures for arrears, with media reports of 10.5% (or ca 80,000) of mortgages in arrears expected in Q1 2012 figures. Of course, given the usual tactic of first exaggerating, then underwhelming (presumably there's some psychological strategy working its magic somewhere here), it should have been expected that actual numbers - bad as they may be otherwise - will 'surprise' to the positive side relative to the leak-related expectations. It might have worked.

Alas, the end numbers - whether or not they are better than leaked out 'estimates' - are pretty dismal.

In Q1 2012, there were 764,138 mortgages outstanding amounting to €112,688.5 million. The latter number is €789 million down on Q4 2011 and€3.27 billion lower than Q1 2011 figure. So in 12 months, with foreclosures and restructuring factored in, Irish mortgagees were able to pay down just 2.82% of the mortgages outstanding. This is not exactly a massive rate of de-leveraging for heavily indebted households.

Of these, 77,630 mortgages were in arrears over 90 days (up 9.4% qoq and 56.5% yoy), with total outstanding amounts of €15,386 million (up 10% qoq and 60.3% yoy). Previous quarter-on-quarter increases were, respectively, 12.7% and 13.1%.

Repossessions in Q1 2012 stood at 961 up from 896 in Q4 2011.

Restructured mortgages:

Alas, the end numbers - whether or not they are better than leaked out 'estimates' - are pretty dismal.

In Q1 2012, there were 764,138 mortgages outstanding amounting to €112,688.5 million. The latter number is €789 million down on Q4 2011 and€3.27 billion lower than Q1 2011 figure. So in 12 months, with foreclosures and restructuring factored in, Irish mortgagees were able to pay down just 2.82% of the mortgages outstanding. This is not exactly a massive rate of de-leveraging for heavily indebted households.

Of these, 77,630 mortgages were in arrears over 90 days (up 9.4% qoq and 56.5% yoy), with total outstanding amounts of €15,386 million (up 10% qoq and 60.3% yoy). Previous quarter-on-quarter increases were, respectively, 12.7% and 13.1%.

Repossessions in Q1 2012 stood at 961 up from 896 in Q4 2011.

Restructured mortgages:

- At the end of Q1 2012, there were 38,658 mortgages restructured, but not in arreas, up 5.06% qoq (against previous qoq rise of 1.16%) and up 5.44% yoy.

- In addition, there were 41.054 restructured mortgages that were in arrears, up 9.23% qoq against previous quarterly rise of 12.67%, and up 56.25% yoy.

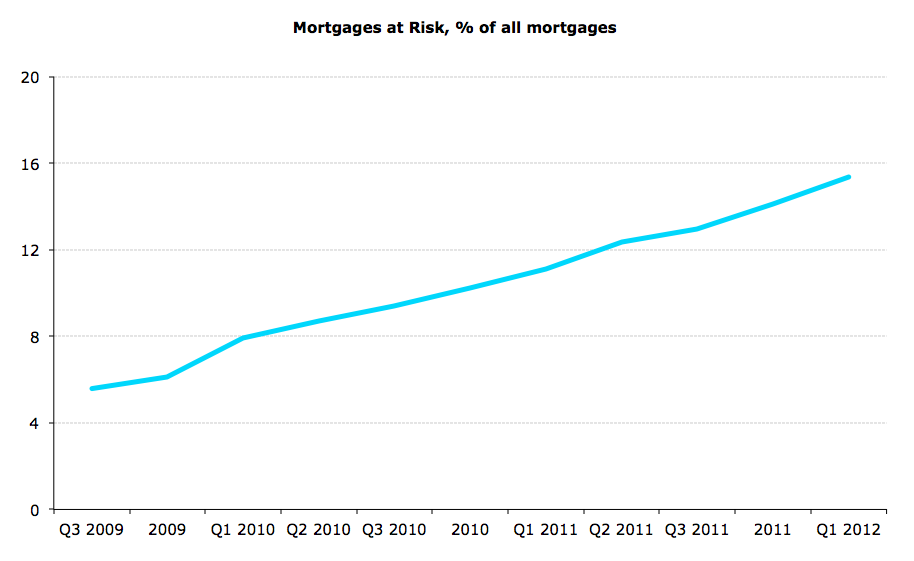

Overall, defining at risk or defaulted mortgages as those mortgages that are currently in arrears (including restructured and in arrears), plus restructured but not in arrears mortgages and repossessions:

- At the end of Q1 2012 there were 117,249 at risk or defaulted mortgages, constituting 15.34% of all mortgages outstanding and amounting to €21.72 billion, or 19.27% of total volume of mortgages outstanding.

- Number of mortgages at risk or defaulted has increased 7.93% qoq in Q1 2012 as compared to a rise of 8.39% qoq in Q4 2011. Annual rise in Q1 2012 was 34.83%.

- Volume of mortgages at risk or defaulted has increased 8.09% qoq in Q1 2012 as compared to a rise of 9.8% qoq in Q4 2011, and there was an annual increase of 37.67%.

- In Q4 2011, mortgages that are at risk or defaulted constituted 14.13% of the total number of mortgages, while in Q1 2011 the proportion was 11.11%, and this rose to 15.34% in Q1 2012.

CHARTS:

Note: more on this next week.

2 comments:

How about this idea

http://www.guardian.co.uk/world/2012/may/27/irish-dodge-debts-uk-bankruptcy-tourism

Its not over yet

Is it possible to get a better breakdown of the numbers ? By calculating a pretty crude percentage of mortgages in trouble over total mortgages subdivided by a timeline doesn't really get to the heart of the issues. What we reqlly require is some sense of when these mortgages originated and their default/stress equally some level (albeit expectedly crude) of negative equity size by origination date. Again this will give readers a better understanding as to the nature of those actually in distress. Broken down by origination date will give everyone a better feel as to what the likely write offs/deals will have to be done to get to the bottom of the issue in terms of right sizing loans and realistic property values. The analysis at the moment is marginally useful but leaves many questions - I would have thought that a better analysis will reveal distress levels in the origonation years from 2003 to 2008 as 3to 4 times the 'average'.

Post a Comment