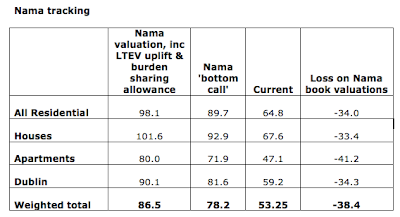

Having looked at the recession/expansion dynamics in Irish economy on foot of Q1 2013 figures (

here), the dynamics in GDP and GNP in Ireland at the aggregate levels (

here), and the mythology of the 'exports-led recovery' (

here), let's round up the Q1 2013 QNA cover with a look at the expenditure-lined components of the GNP and GDP.

Below we look at the Seasonally-adjusted Current Market Prices data.

Personal Expenditure on Consumption Goods and Services fell 2.21% in Q1 2013 q/q and was up 0.01% y/y. This compares against much more benign drop of -0.07% q/q in Q4 2012 and a 1.15% rise y/y. Since Q1 2011, when the Coalition came to power, Personal Expenditure is down 1.55%. In terms of q/q changes, Q1 2013 marked second consecutive quarter of declines.

Net Government Expenditure on Current Goods and Services declined 0.1% q/q in Q1 2013 and was down 2.56% y/y. This marks moderation in declines recorded in Q4 2012 when q/q decline stood at -1.90% and y/y decline was running at -2.88%. Net Government Expenditure decline was the shallowest contributor to voerall economic contraction recorded in Q1 2013. Compared to Q1 2011, Net Government Expenditure on Current Goods & Services was down 3.98% in Q1 2013. In terms of q/q changes, Q1 2013 marked second consecutive quarter of declines.

Gross Fixed Capital Formation - the most devastated expenditure component of GNP to-date has fallen massive 7.32% in Q1 2013 in q/q terms and was down whooping 18.74% in y/y terms. This shows dramatic acceleration in decline from -2.16% drop in q/q terms in Q4 2012 and the reversal of the y/y rise of +4.31% recorded in Q4 2012. Relative to Q1 2011, Gross Fixed Capital Formation was down 14.25% in Q1 2013. In q/q terms, Q1 2013 marked second consecutive quarter of declines.

Exports excluding factor income shrunk 0.79% in Q4 2012 on q/q basis and there was 4.93% growth in y/y terms. This was then. In Q1 2013 exports of goods and services fell 4.59% q/q and were down 3.13% y/y. Relative to Q1 2011 exports of goods and services net of factor income payments were up 2.22% in Q1 2013, but we also marked two consecutive quarters of contraction here.

Imports of goods and services, net of factor income payments were down 2.12% q/q in Q1 2013 and -3.13% y/y. This marks significant shift 'South' in the series compared to Q4 2012 when imports shrunk 1.05% q/q and were up 4.57% in y/y terms. Imports are running -0.05% down on Q1 2011 and Q1 2013 marks the second consecutive quarter of q/q declines.

GDP at curent prices, seasonally adjusted fell 0.6% q/q in Q4 2012 and there was annual growth of 0.38%. In Q1 2013, GDP fell 2.16% q/q and there was annual decline of 2.09%. This marks third consecutive quarter of decline in GDP and thus officially, return of the recession is dated to Q4 2012. The average rate of recessionary decline in GDP in the current episode is so far -1.06% per quarter. This is shallower than the previous recessionary episode (Q4 2008-Q4 2009) when GDP contractions averaged 2.76% per quarter. Compared to Q1 2011, Q1 2013 GDP at current market prices stood at -1.04%, or put differently, gross domestic product in Ireland in Q1 2013 stood below the levels attained in Q1 2011 when the current Government came to power.

Net factor income from the rest of the world declined in both Q4 and Q1, with decline accelerating in Q1 2013 to 19.21% q/q from 2.92% in Q4 2012. As the result of this, GNP moved up, in the opposite direction of the GDP.

GNP at current market prices grew 0.68% q/q in Q1 2013, down on 1.18% expansion recored in Q4 2012. On y/y basis, GNP grew 4.12% in Q4 2012 and by 4.26% in Q1 2013. Compared to Q1 2011, GNP is now up 2.46%.

Both

Final Domestic Demand and

Total Domestic Demand posted second consecutive quarter of q/q contraction in Q1 2013.

To summarise,

not a single line of expenditure posted an increase in the Q1 2013 in terms of q/q changes once seasonal adjustments are taken into the account. In other words, the sole positive improvement in the numbers - relating to GNP - was driven

exclusively by reduced outflow of funds from MNCs.

Worse, not a single line in the determination of the GDP in Ireland was up in q/q terms in any quarter since the end of Q3 2012. We had, put differently, 6 months of across the board contractions in the economy, when we consider expenditure-based definition of GDP.