Here's my Sunday Times article from May 20, 2012. Unedited version, as usual.

Welcome to the terminal stage of the Euro crisis. Only two

years ago European press and politicians were consumed with the terrifying

prospects of a two-speed Europe. This week, preliminary estimates of the Euro

area GDP growth for the first quarter of 2012 have confirmed that the common

currency area, instead of bifurcating, has trifurcated into three distinct

zones.

In the red corner, we have the pack of the perennially

struggling economies of Cyprus, Greece, Italy, Portugal and Spain. The

Netherlands, with annual output contraction of -1.3% in Q1 2012, matching that

of Italy, has quietly joined their ranks. These countries all have posted

negative growth over the last six months if not longer. Cyprus, Italy, and

Portugal, alongside the Netherlands, registering negative growth over the last

three quarters. Ireland and Malta, two other candidates for this group are yet

to report their Q1 2012 results, with the former now officially in a recession

since the end of 2011, while the latter having posted its first quarter of

negative growth in Q4 2011.

In the blue corner, Belgium, France, and Austria all have

narrowly missed declaring a recession in the last quarter, while posting 0.5%

annual growth or less.

Lastly, in the green corner, Estonia, Finland, Germany and

Slovakia have served as the powerhouse of the common currency area, pushing the

quarterly growth envelope by between 0.5% and 1.3%.

The red corner accounts for 40% of euro area entire GDP, the

blue corner – for 29%. All in, less than one third of the euro area economy is

currently managing to stay above the waterline.

Looking at the picture from a slightly different

prospective, out of the Euro 4 largest economies, France has shown not a single

quarter of growth in excess of 0.3% since January 2011. In the latest quarter

it posted zero growth. Germany – the darling of Europe’s growth strategists –

has managed to deliver 0.5% quarterly growth in Q1 2012 on foot of 0.2%

contraction in Q4 2011. Annual growth rates came at an even more disappointing

1.2% in Q1 2012, down from 2.0% in Q4 2011. Italy decline accelerated from

-0.7% in Q4 2011 to -0.8% in Q1 2012, while Spain has officially re-entered

recession with 0.3% contraction in Q4 2011 and Q1 2012.

The Big 4 account for 77% of euro area total economic

output. Not surprisingly, overall EA17 growth was zero in Q1 2012 both in

quarterly terms and annual terms. The latest leading indicator for euro area

growth, Eurocoin, reading for April 2012 shows slight amplification of the

downward trend from March. In other words, things are not getting better.

The best countries in terms of overall hope of economic

recoveries – net exports generators, such as Austria, Belgium, Ireland, and the

Netherlands, are all stuck in either the twilight zone of zero growth or in a

years-long recession hell.

Ireland’s exporting sectors have been booming, with total

exports rising from the recession period trough of €145.9 billion in 2009 to

€165.3 billion in 2011. However, the rate of growth in our exports has been

slowing down much faster than projected for 2012. If in 2010 year on year total

exports expanded 8.1% in current prices terms, in 2011 the rate of growth was

4.8%. Our overall trade surplus for both goods and services grew 12.8% in 2011

– impressive figure, but down on 19.7% in 2010.

So far this year, the slowdown continues.

The latest PMI data suggests that manufacturing activity is

likely to have been flat in Q1 2012. Latest goods exports data, released this

week, shows that the sector posted zero growth confirming overall readings from

the PMI. The value of trade in goods surplus steadily declined since January

2012 peak of €3,813 million to €3,023 million in March 2012, and in annual

terms, Q1 2012 surplus for merchandise trade is now down €99 million on 2011.

Although the quarter-on-quarter reduction appears to be small due to relatively

shallow trade surplus recorded in January 2011, March seasonally-adjusted trade

surplus is down 22% or €850 million on March 2011. With patents expiring, the latest data shows

that exports of Medical and pharmaceutical products fell €772 million in Q1

2012 compared to Q1 2011. Overall, comparing first quarter results, 2011

registered seasonally-adjusted annual growth of 7.9% in exports and 15.2% in

trade surplus. 2012 Q1 results are virtually flat, with exports rising 0.03%

and trade surplus rising 0.8%.

Looking at the geographical composition of our merchandise

trade, until recently, our exports and trade surplus were strongly underwritten

by re-exportation by the US multi-nationals into North America of goods

produced here. This too has changed in Q1 2012, despite the fact that the US

has managed to stay outside the economic mess sweeping across Europe. In three

months through March 2012, Irish exports to the US have fallen 19.3% and our

trade surplus with the US has shrunk 47.1% from €3.33 billion to €1.76 billion.

Services are more elusive and more volatile, with CSO

reporting lagging the data releases for goods trade, but so far, indications

are that services activity remained on a very shallow growth trend through Q1

2012. As in Manufacturing, Services demand has been driven once again by more

robust exports, and as for Manufacturing, this fact exposes us to the potential

downside risk both from the on-going euro area crisis and from the clear

indication that our domestic economy continues to shrink even after an already

massive four years-long depression.

No matter how we spin the data, the reality is that exports

generation in Europe overall, and in Ireland in particular, is still largely a

matter of trade flows between the slower growth North American and European

regions.

In many ways than one, Ireland is a real canary in the mine,

because of all Euro area economies excluding the Accession states, Ireland

should be in the strongest position to recover and because our exporting

sectors continue to perform much better than the European average. Yet the recovery

is nowhere to be seen.

Instead, the growth risks manifested in significant slowdown

in our external trade activity and in overall manufacturing and services

sectors are now coinciding with the euro entering the terminal stage of the

crisis.

Since the beginning of this week, Belgian and Cypriot,

Austrian and Dutch, virtually all euro area bonds have been taking some

beating. In the mean time, credit downgrades came down on Italy and Spain, and

the Spanish banking system was exposed, at last, as the very anchor that is

likely to drag Europe’s fifth largest economy into EFSF/ESM rescue mechanism.

This week, in a regulatory filing, Spain’s second largest bank, BBVA stated

that: “The connection

between EU sovereign concerns and concerns for the health of the European

financial system has intensified, and financial tensions in Europe have reached

levels, in many respects, higher than those present after the collapse of

Lehman Brothers in October 2008.” Meanwhile, Greek retail banks have lost some

17% of their customers’ deposits since mid-2011 and this week alone have seen

the bank runs accelerating from €700 million per day on Monday-Tuesday, to over

€1.2 billion on Wednesday.

This

is not a new crisis, but the logical outcome of Europe’s proven track record of

inability to deal with the smaller sub-component of the balance sheet recession

– the Greek debt overhang. Three years into the crisis, European leadership has

no meaningful roadmap for either federalization of the debts or for a full

fiscal harmonization. There is no growth programme and the likelihood of a

credible one emerging any time soon is extremely low. Structural reforms are

nowhere to be seen and productivity growth as well as competitiveness gains

remain very shallow, despite painful adjustments in private sector employment

and wages. Inflation is running well above the targets. Austerity is nothing

more than a series of pronouncements that European leaders have absolutely no

determination to follow through. EU own budget is rising next year by seven

percentage points, while Government expenditure across the EU states is set to

increase, not decrease.

In

short, three years of wasteful meetings, summits, and compacts have resulted in

a rather predictable and extremely unpleasant outcome: aside from the ECB’s

long term refinancing operations injecting €1 trillion of funds into the common

currency’s failing banking system, Europe has failed to produce a single

meaningful response to the crisis.

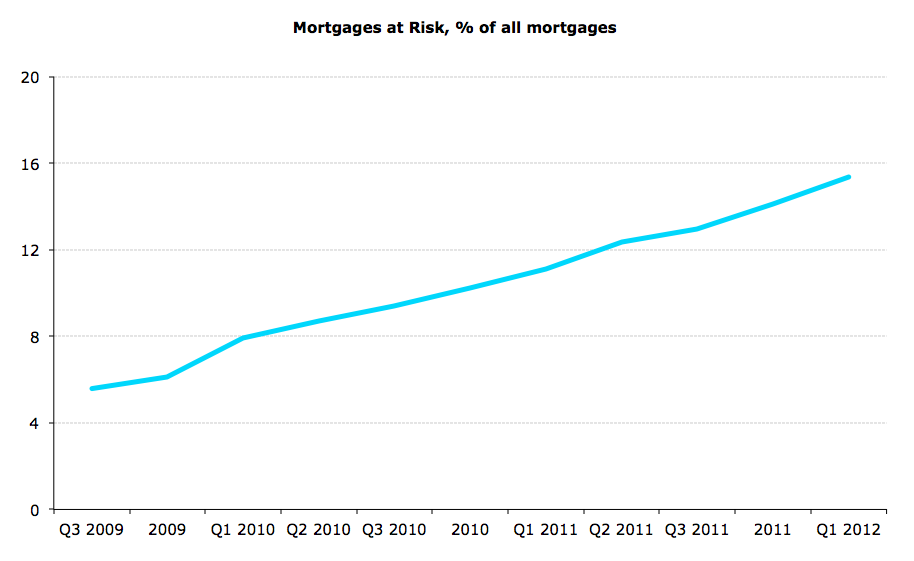

CHARTS:

Box-out: Speaking at this week’s conference of the

Irish economy organized by Bloomberg, Department of Finance Michael Torpey has

made it clear that whilst one in ten mortgagees in the country are now failing

to cover the full cost of their loans, strategic defaults amount to a

negligible percentage of those who declare difficulty in repayments. This

statement contradicts the Central Bank of Ireland and the Minister for Finance

claims that the risk of strategic defaults is significant and warrants shallow,

rather than deep, reforms of the personal bankruptcy code. Furthermore, the

actual levels of mortgages that are currently under stress is not 10% as

frequently claimed, but a much higher 14.1% - the proportion corresponding to

108,603 mortgages that have either been in arrears of 30 days and longer, or

were restructured in recent years and are currently not in arrears due to a

temporary reduction in overall burden of repayments, but are at significant

risk of lapsing into arrears once again. The data, covering the period through

December 2011 is likely to be revised upward once first quarter 2012 numbers

are published in the next few weeks. In brief, both the mortgages arrears

dynamics and the rise of the overall expected losses in the Irish banking

system to exceed the base-line risk projections under the Government stress

tests of 2011 suggest that the state must move aggressively to resolve

mortgages crisis before it spins out of control.