An excellent article in the Irish Examiner today on the state of our economy as contrasted by the state of our PR/spin machine: http://www.irishexaminer.com/opinion/columnists/colette-browne/enda-needs-to-be-a-better-salesman-when-flogging-economic-recovery-pitch-224593.html

Wednesday, March 6, 2013

6/3/2013: Reality v PR Spin - Irish Economy

An excellent article in the Irish Examiner today on the state of our economy as contrasted by the state of our PR/spin machine: http://www.irishexaminer.com/opinion/columnists/colette-browne/enda-needs-to-be-a-better-salesman-when-flogging-economic-recovery-pitch-224593.html

Tuesday, March 5, 2013

5/3/2013: Irish trade with BRICs: 2004-2012

Four charts on Irish bilateral goods trade with Bric countries:

5/3/2013: Another Consumer Confidence Report Goes Off-Road

To the 'turning around' reports from the Eastern Front ca 1943... err... 2013... per KBC Ireland/ESRI Consumer Sentiment Index, consumer sentiment in Ireland fell in February to 59.4 compared to January reading of blistering 64.2. The report gets 'serious' on dynamics: "The three-month moving average also decreased from 59.3 to 57.8. The index fell below the average for the last 12 months (61.9)."

Let me add some more dynamics to this. First, let's look at January 2012 data (since we do not have Retail Sales Indices for February yet):

- Current 3mo average for Retail Sales Value Index is 96.8, down from 96.9 for 3mo average through October 2012, Volume is up from 100.3 to 100.5. Overall, indices are basically flat (+/-0.1% is not a significant change by anyone's standards, even for this Government);

- 3mo average of Consumer Confidence index through January 2013 was 59.3 down on 63.7 for the 3 months though October 2012.

- 6mo average, however, shows a slightly different story: Value of sales is up from 95.3 average reading for 6 months through June 2012 to 96.8 average for 6 months through December 2012; Volume is up from 98.8 to 100.4 over the same period, and Consumer Confidence is up from 105.8 to 107.7.

KBC/ESRI Consumer Sentiment Index is about as good of a gauge for retail sector activity here as the elephants' herd gate tempo is of use for timing the Swan Lake pas de deux. If you don't believe me, here's a chart:

In the nutshell, consumer confidence hit the bottom in July 2008 and since then things were, apparently improving. So much so that by June 2012 Value of Retail sales has hit the absolute record low, whilst Volume of sales did same in October 2011. There is a gentle uptrend in consumer confidence since mid-2008 against a downtrend in both Volume and Value of core retail sales.

Taken on 3mo average basis (to cut down on volatility), Confidence indicator has virtually nothing to do with Retail Sales, except for high sounding press release comments from the experts:

Per ESRI: "The promissory note deal was announced roughly half way through the survey period. The announcement of the deal would appear to have had some positive impact, with a preliminary analysis of responses showing an improvement in sentiment after the deal. We await the March results to see if the impact on sentiment is sustained.”

Indeed, we await... eagerly.

In addition, Austin Hughes, KBC Bank Ireland, noted that [comments are mine] “A disappointing aspect of the sentiment data for February was that the decline was broadly based. Consumer spending power remains under pressure and there is little to suggest a dramatic improvement in Irish economic circumstances that would cause a ‘feel good’ factor to emerge anytime soon. [A revelation of most profound nature]

"About the best that can be expected is a slow easing in the ‘fear factor’ that would encourage a gradual increase in spending. This may not be spectacular but it still represents significant progress. [What progress he might have in mind beats me, as Retail Sales figures continue to show little signs of reviving from already abysmally low levels]

"...The Irish consumer is seeing an improvement in ‘macro’ conditions across the economy but their personal finances remain under pressure. [In other words, we are in that ESRI & KBC-lauded 'exports-led recovery' boom, folks, where you and I get screwed, while MNCs get to report greater 'sales']

"It may be that some consumers had unrealistic expectations as to what a deal could achieve. [Did Government enthusiasm in over-selling the potential impact propelled enthusiasm of consumers for the 'deal'?]

"More generally, it remains the case that consumers face significant further austerity in the next two Budgets. [Doh! We'd be discovering new Solar Systems, next]

"The deal may ease the pain somewhat but it doesn’t entirely remove it. So, we shouldn’t expect a surge in confidence. That said, the fragile situation of Irish consumers means they are sensitised to bad news. So, failure to reach a deal could have seen sentiment deteriorate quite sharply.” [In other words, we were saved from an apocalyptic collapse of consumer confidence by the wisdom and the heroic efforts of the Government... and ATMs are still working!]

Irony has it, the same 'positive newsflow' that went along with the index slide this time around also supported (according to the authors) index surge in January - see here for January release comments: http://www.kbc.ie/media/CSI.Jan20131.pdf Who says you can't have a cake and eat it at the same time?

I don't know what to do - laugh or cry... cup of coffee is needed, however, as much as some serious improvements in survey to bring it closer to reality on the ground. It is needed because:

- While Consumer Confidence index through January 2013 (to take period consistent with data availability for both Retail Sales Indices and Consumer Confidence Index) was up 13.4% y/y, while actual retail sales rose just 0.94% in Value and 0.71% in Volume.

- Compared to 2005 average, Retail Sales Value was down 3.42%, Volume was down 0.22% and Consumer Confidence was up 26.82%.

- Even with February 2013 moderation, Consumer Confidence is now up 17.33% on 2005 average.

- Worse than that, taking Crisis Period averages (January 2008-present), Value of Retail Sales is now running at 96.6 against the average of 101.17 (or 4.51% below average), Volume at 99.8 against the average of 103.49 (or 3.56% below average), whilst Consumer Confidence is running at 7.37% above the Crisis Period average of 55.32.

5/3/3013: Irish Services PMIs: February 2013

Irish Services PMI (published by NCB) for February were out today, highlighting some interesting (for a change) shifts in the short-term trends worth discussing.

The headline numbers were good, although less strong than those recorded in January. This is not surprising since PMI surveys are biased toward multinationals in some core driving sectors (due to weighting factors attached to sectors and the overall quality, collection and reporting of data biases).

The headline numbers were good, although less strong than those recorded in January. This is not surprising since PMI surveys are biased toward multinationals in some core driving sectors (due to weighting factors attached to sectors and the overall quality, collection and reporting of data biases).

- Seasonally-adjusted Business Activity (headline index) declined to 53.6 in February from 56.8 in January 2013, but remained above 50.0 line.

- 12mo MA through February 2013 was 53.0, which is not statistically significantly different from 50.0, but nonetheless represents a reading consistent with moderately strong expansion of activity. This marks the seventh consecutive month of readings above 50.0 although February was the second slowest month for activity over this latest period of consecutive expansions.

- 3mo MA through February is now identical to the previous 3mo MA through November 2012 - both at 55.4. For comparative purposes: 3mo MA through February 2010 was 47.2, through February 2011 - 52.1, through February 2012 - 50.0, so annualised activity is running ahead of previous 3 years.

- Main point to be made in the above is that since roughly April 2010, we have been trending along a new late- or post-crisis trend along the average of 52.1 average (49.6 to 54.6 range) as compared to May 2000-December 2007 average of 57.6 (52.5 to 62.7 range). As charts above and below clearly show, the new trend is (1) lower and (2) less steep in take-offs from the local minima (lows). In my view - this shows two factors: Factor 1: overall slower rate of growth (do keep in mind that the current trend is coming off historical lows of the Great Recession and should be consistent with much faster uplift and higher average and range than pre-crisis trend), and Factor 2: more mature nature of business in Irish Services sectors (with ICT and Financial Services now in advanced stages of late investment cycle compared to the period of 2000-2007 when these were growing rapidly and posting recovery from the dot.com bubble).

Now on to some of the components of the headline index.

- Chart above shows that New Business sub-index also posted moderation in the rate of growth in February 2013 compared to five months of robust expansion prior to February. In fact, February reading of 53.1 was the slowest pace of expansion in seven months, although it does come on foot of seven months of consecutive above 50.0 readings.

- Trend-wise, the same conclusions that were drawn in the last bullet point on the headline index - those relating to structurally slower pace of growth in the recent years compared to pre-crisis rates of expansion - continue to hold for New Business sub-index as well. Since April 2010, the sub-index averaged 51.3 (range of 48.4 to 54.2) against pre-crisis (May 2000-December 2007) average of 57.4 (range of 52.4 to 62.5).

- On short-term dynamics, 3mo MA through February 2013 stood at 55.4, slightly down on 55.8 3mo MA through November 2012, but ahead of 47.2 3mo MA through February 2010, ahead of 52.1 3mo MA through February 2011 and ahead of 50.2 3mo MA through February 2012.

Chart below summarises the shorter-range data for the two core indices.

Two charts plotting other principal components of the overall index:

Focusing on few sub-series of interest:

- Employment sub-index remained above 50.0 in February, posting a reading of 52.5 - the shallowest expansion since September 2012, but marking a sixth consecutive month above 50.0. 3mo MA now is at 54.1 and previous 3mo MA through November 2012 was at 53.0. Good news - in 2009-2012 3mo MA through February was below 50.0 in every year. Bad news is that Employment is closely linked with Profitability (see below).

- Business Confidence / Expectations 6mo out are continuing to fly high, propelled most likely by a combination of current upbeat conditions (the two series: Expectations and Current Conditions show the strongest co-determining relationship of all series, suggesting that the real driver for Expectations is not actual anticipation of the future events, but rather firms' assessment of current conditions) and by the endless barrage of feel-good propaganda from the business lobby and the State. The last, third factor, is human nature (aka 'winner's curse' bias). We expect things to get better because they were pretty damn awful until now and for a very long time... Come on, folks, let's face the music - unless you are a transfer-pricing arbitraging MNC, things are hardly getting any better. And, unless you live in the world of Googlites (aka 25-30 year olds with no attachment to anything save a party on a weekend) you are facing a mountain of debt, shrinking assets and wealth, higher taxes and the prospect of more of the same. What 'confidence at 69.1' can we have in mind?

- Oh, and to top things up - you'd think that Confidence comes from higher profits for the firms... Well, in the Wonderland of Transfer Pricing it is not and hence in Ireland we have Services sector where profitability is shrinking (41.5 in February on 49.2 in January) for 62 consecutive months now (since January 2008, every month there was negative profitability growth, with the average shrinkage at 41.9 - aka very very very deep contraction), but businesses confidence has been up on average at 60.9 - aka very very strong confidence growth on monthly basis).

If anything, aside from the major trend outlined in the first set of bullet points above, the point on Confidence and Profitability is the second main conclusion from the longer-term data analysis, for it exposes the surreal nature of the Irish economy - economy distorted by extreme transfer pricing and tax optimisation activities of the MNCs.

Now, let's touch briefly on the main short-term observation from today's data release: the core drivers for each of the main sub-series:

- When it comes to Business Activity index, level support at 53.6 in February was provided by a broader base of sectors, with Technology, Media & Telecoms sector (TMTS) posting comparable expansion to Transport, Travel, Tourism & Leisure sector (TTTLS). This is similar to what was observed back in October 2011 and is an improvement on the trend that (at least over the last six months) have seen TMTS being the main and dominant driver of the index improvements.

- Business Activity Index for Expectations out 12 months ahead was dominated (as in every one of the previous 6 months) by TMTS, with Business Services Index coming in as the second upside driver (same as in January 2013).

- TMTS was the main driver for the third consecutive month behind growth in Incoming New Business, while Financial Services were the main driver over the last 4 months behind the growth in the Incoming New Export Business.

- In Employment generation, TMTS again outstripped all other sectors for the third consecutive month, which, of course, means we are only reinforcing the demographic misalignment emerging in the economy with main generation of new jobs taking place in sectors that are more reliant on importing skills from abroad.

- TMTS was the only sector in which profitability improved in February 2013 (same as in December 2012 and January 2013). In all other sectors, profitability was in decline for the third consecutive month. Why, you might ask? Interestingly, TMTS saw the sharpest countermovement in input/output prices, with input costs posting sharpest acceleration in February, and output costs posting the sharpest deterioration. In any normal economy that would mean shrinking, not expanding, profit margins. But in Ireland, of course, there is little normal about the TMTS sector dominated by the massive MNCs aggressively using their Irish activities for tax arbitrage from their European and even global operations.

Some interesting stuff, eh? You bet official 'analysis' of Irish PMIs is not talking about any of this...

5/3/2013: Charts to Keep You Awake at Night

Bragging rights alert...

Business Insider published their slide deck of charts that keep investment community awake at night... The full 'horror show' is on here: http://www.businessinsider.com/wall-streets-most-worrying-charts-2013-3#

I have contributed the following chart: http://www.businessinsider.com/wall-streets-most-worrying-charts-2013-3#constantin-gurdgiev-trinity-college-dublin-37

Sunday, March 3, 2013

3/3/2013: Global Economic Outlook - economists' consensus

BlackRock Investment Institute published a summary of the views of over 430 economists from more than 200 institutions, spanning over 50 countries that form the BlackRock Investment Institute's Economic Cycle Survey Panel. It is worth stressing that:

1) These are not the views of the Institute, but the views of the Panel, and

2) Since the Panel is still in the process of built up, some countries have 'thin' coverage - with small number of respondents specialising in the specific country analysis.

The aggregate view from the most recent round of surveys is presented below (due to size limitations, it is probably best to view this as a separate image, so double click on the image below):

3/3/2013: Some recent links on Science funding in Ireland

Recent changes to the Irish State funding for scientific research and the hatchet job of 'restructuring' the policy formation mechanisms for science funding and development have been in the newsflow for some time.

Here are a couple of very good links relating to the matter:

Here are a couple of very good links relating to the matter:

- One superb post: The Link between Research and Education http://wp.me/p2ycg5-5r | Exposes fundamental flaws in the new Irish Science funding model

- An article on stem cell research in medicine exposes more failings at the policy level, contrasting with the progress in the actual field: http://medicalindependent.ie/22847/the_stem_cell_revolution

- Very strong article on fiscal side of the equation of funding science: http://www.finfacts.ie/irishfinancenews/article_1025627.shtml

- And one quite 'would funny if it weren't tragic' interview with our 'Hands-on-Scientists' Minister attempting to explain that scientists are wrong on just how right he himself is: http://www.irishexaminer.com/ireland/sherlock-denies-science-role-clash-223295.html

- Quick blogpost showing that our 'Hands-on-Scientists' Minister is just a bit off target when it comes to his own Government policy formation structures: http://sciencecalling.com/2013/02/19/foi-reveals-new-information-about-csa-role/#more-5268

- And a strongly-worded challenge to the Minister's deep thoughts: http://loveirishscience.wordpress.com/2013/02/19/an-embarrassing-rant-by-the-minister-for-research-and-innovation/

- The original interview in which the Minister is labeling scientists 'children' and 'liars' - which has since been removed, but is worth visiting if only to witness the degree of State interference with the media: http://www.broadsheet.ie/2013/02/18/liars-and-children/ and here it is with the bits of quotes: http://sciencecalling.com/2013/02/18/policy-speak/

Of course, in fairness to the Irish Government, Europe-wide 'Smart Economy' and 'R&D-intensive growth' leaders are also slashing funding for research http://www.nature.com/news/europe-s-leaders-slash-proposed-research-budget-1.12403 . Maybe burning books will be our next pass-time, offering the economically uplifting marshmallows over a flaming Group Homology tome, anyone?

Friday, March 1, 2013

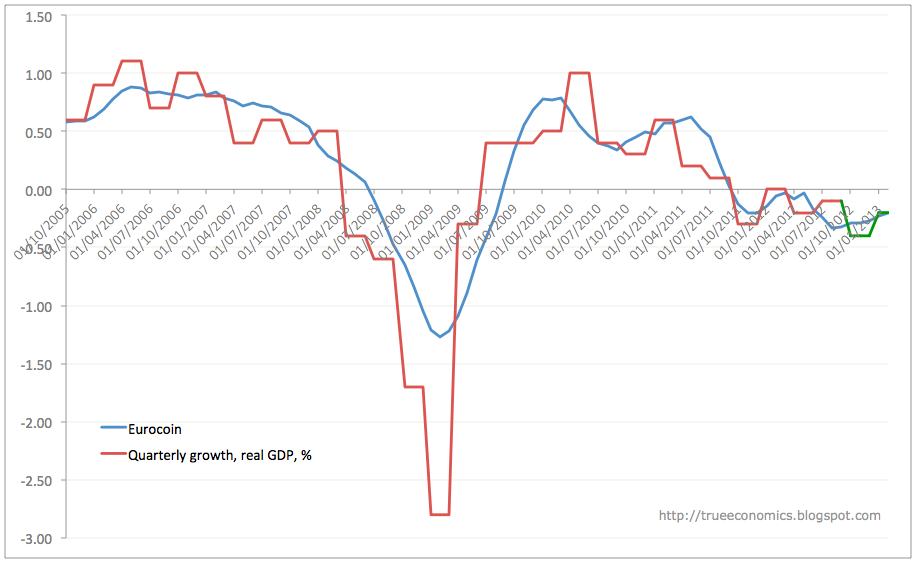

1/3/2013: Eurocoin February 2013 - 17 months-long recession?

February eurocoin leading growth indicator for the euro area, published by the Banca d'Italia and CEPR came in at another sub-zero reading of -0.20. This marks statistically insignificant improvement from -0.23 in January 2012.

More ominously, the reading posts 17th consecutive monthly below-zero reading. Put differently, on monthly average basis, eurocoin has been posting sub-zero readings since March 2011.

Y/y comparatives are even worse. Back in February 2012 the indicator stood at -0.06, and in February 2011 it was running at a blistering pace of +0.57, while in February 2010 we had a reading of +0.77. In fact, this is the lowest reading for any February since the depths of the Great Recession in February 2009.

Two charts to illustrate the eurocoin dynamics and associated implied growth forecasts:

As I pointed out before, the last 12 months of economic performance in the euro area have shown very clearly that the ECB monetary policy stance is not working. Here are the same illustration (updated to February 2013 figures) once again:

Growth-consistent level of the ECB rates is zero. Meanwhile, with slowly moderating inflation still above the target, inflation-consistent rates are probably closer to 1.25-1.5%.

Inexistent fiscal policy at the euro area level is matched by the dysfunctional monetary policy. Next stop? Possibly political psychosis?

More ominously, the reading posts 17th consecutive monthly below-zero reading. Put differently, on monthly average basis, eurocoin has been posting sub-zero readings since March 2011.

Y/y comparatives are even worse. Back in February 2012 the indicator stood at -0.06, and in February 2011 it was running at a blistering pace of +0.57, while in February 2010 we had a reading of +0.77. In fact, this is the lowest reading for any February since the depths of the Great Recession in February 2009.

Two charts to illustrate the eurocoin dynamics and associated implied growth forecasts:

- 3mo MA is now at -0.233, while 6mo MA is at -0.267. 2008-2009 crisis-period average was -0.31. Draw your own conclusions (STDEV = 0.471 for historical record and 0.560 for the crisis period).

As I pointed out before, the last 12 months of economic performance in the euro area have shown very clearly that the ECB monetary policy stance is not working. Here are the same illustration (updated to February 2013 figures) once again:

Growth-consistent level of the ECB rates is zero. Meanwhile, with slowly moderating inflation still above the target, inflation-consistent rates are probably closer to 1.25-1.5%.

Inexistent fiscal policy at the euro area level is matched by the dysfunctional monetary policy. Next stop? Possibly political psychosis?

Thursday, February 28, 2013

28/2/2013: Boring, Boring Property Prices in January

When one is bored, truly deeply bored, it is hard to muster much strength to go through the twists and turns of the data. And I am bored, folks. Irish property prices data, released by CSO today, is simply equivalent to watching a fish flopping on hot asphalt - it is simply, clearly, obviously, patently... not going anywhere.

That is the story with the stats from Ireland nowadays - the flatline economy, punctuated by the occasional convulsion up or down.

Alas, to stay current we simply have to go through the numbers, don't we?

Let's first do a chart. Annual series for 2012 are finalised and were revised slightly down on the aggregate index compared to the previous release:

The chart clearly shows that despite all the talk about 'bottoming out' house prices, and 'buyers throwing deposits on unfinished homes' is a quasi-2006 frenzy, property prices in Ireland fell over the full year 2012.

Recall the prediction by some economists that property prices are likely to stabilise around -60% mark on peak? I made similar claim, but referencing in the medium term Dublin and larger urban areas, while stating that nationwide prices will be slower to react due to rural and smaller towns' property markets being effectively inactive. Guess what? Dublin prices were down 56.3% on peak in 2012. Not exactly that badly off the mark. Apartments prices - down 61.1% on peak. Exceeding the mark. Nationwide, properties were down 49.5% on peak, still some room to go, but in my view, we are still heading in the direction of 60% decline.

Now, onto monthly series.

Nationwide Property Prices:

- All properties RPPI declined from 65.8 in December 2012 to 65.4 in January 2013 (down 0.61% m/m) and is down 3.25% y/y.

- Despite all the 'stabilisation claims', overall RPPI has not posted a single month y/y increase since January 2008.

- The 'good news' is that RPPI rate of decline (in y/y terms) has slowed down for the 9th consecutive month in January 2013.

- 3mo MA has been static now over the last 3 months at 65.77, which simply means that half of the gains that were made from the historical trough of 64.8 in June 2012 to the local peak of 66.1 attained in November 2012 were erased when the index fell to 65.8 in December. January rise is a tiny correction back up.

- Let's put this differently. January 2012 index returned us back exactly to the level of prices recorded in April 2012 and then repeated in October 2012.

- The market is... lifeless. Irony has it: 3mo cumulated gains through December 2012 were exactly zero. 3mo cumulated change in the index through January 2012 is exactly zero.

- 6mo cumulative gains are more 'impressive' at +0.77%.

- But put this into perspective: this rate of 'growth' implies annualised rate of +0.878%. At this rate of annual expansion, the next time we shall see 2007 peak level prices for properties, expressed in nominal terms, will be 2092.

Dublin:

- Prices in Dublin corrected slightly up in January to 59.5 from 59.2 in December 2012. Latest reading is still below 60.0 local peak recorded in November 2012, so the correction is so far very much partial.

- Y/y prices are now firmer at +2.06% in January, having posted -2.47% decline in December. January marked the first month that we had y/y increases in prices since November 2007.

- The rate of price increase in January in y/y terms, however, is basically solely correcting for inflation, which means that for anyone with a mortgage payable today, property 'wealth' is continuing to drop in real terms. Obviously, that is too far advanced of an analysis for the Government and its cheerleaders who think 2.06% increase in just one month over 62 months is a firm sign of a 'turnaround' or worse, 'recovery'.

Instead of boring you with the discussion of detailed stats on dynamics, here are the main charts:

All of the above show basic reality of an L-shaped 'recovery' we have been having to-date. May be, one might hope or one might dread, the prices will move up from here in a more robust fashion. Reality is - so far, they are not... When that reality changes, I will let you know.

28/2/2013: Risk-free assets getting thin on the ground

Neat summary of the problem with the 'risk-free' asset class via ECR:

Excluding Germany and the US - both with Negative or Stable/Negative outlook, there isn't much of liquid AAA-rated bonds out there... And Canada and Australia are the only somewhat liquid issuers with Stable AAA ratings (for now). Which, of course, means we are in a zero-beta CAPM territory, implying indeterminate market equilibrium and strong propensity to shift market portfolio on foot of behavioural triggers... ouchy...

Tuesday, February 26, 2013

26/2/2013: 'Italy effect"

Mid-day 'Italy effect' or may be 'democracy effect' or 'No Goldie Sachs Boy in Rome effect'? CDS markets (via CMA) the EU has not banned... yet

Also, note that everyone in the periphery is being clubbed: Ireland and Portugal inclusive (we can safely assume that Tunisia, Sweden, Russia and Bulgaria have been coupled into the group on ad hoc bases).

26/2/2013: The Real Lesson from Italian Elections

The outcome of the Italian elections is the current core driver of the newsflow. Alas, so far, it is for a very wrong reason. The Italian voters have returned a divided Legislature, prompting the claims that Italy is now at a risk of becoming 'ungovernable'. In reality, such statements are confusing one of the symptoms for the entire disease because the original departing assumption of the analysts arguing such a scenario is that the brief period of technocratic governance under Mario Monti administration was:

- Effective in enacting / implementing reforms,

- Involved reforms needed to address the core problems faced by Italy, and

- A sustainable 'new normal' for Italy.

In fact, none of the above three assumptions are valid.

Firstly, the reforms enacted by Mario Monti administration were shallow, not structural and addressed the issue of deficits (which are not the core problem for Italy). These reforms were successfully resisted on the ground - with exception of few tax measures, which were all regressive to growth and were unlikely to survive intact into the future due to their unpopularity as much as due to the fact that Italians evolve very systemic tax evasion responses over time to virtually all attempts to claw tax out of the real economy. There is also a pesky problem that Italian tax burdens are already very high, creating disincentives to entrepreneurs and highly skilled.

Secondly, the reforms enacted by Monti were not addressing the main two problems faced by Italy: the gargantuan Government debt, and the decades-long period of economic stagnation. Structurally, Monti reforms were like a plaster applied to a shark wound, helping to lower the cost of funding the state, but changing little in terms of what is being funded, why it is being funded, and how it is being funded.

Thirdly, technocratic regime is simply incompatible with democratic institutions, and as such cannot be sustained. The result of the latest election actually show the deep disconnect between professional capability of the state / business managerial elites (Monti) and political leadership (ideas-light, and thus forced into rhetorical campaigns juxtapositions) that is emblematic of the proceduralist, bureaucratised European modus operandi since the 1960s.

Europe's political elite - thin on ideas, experience of real management and knowledge - is incapable of defining leadership beyond populism. Meanwhile, Europe's professional elite - permanently shielded from reality of life by protectionism and bureaucratic licenses - is incapable of capturing hearts & minds of any electorate, let alone emotive electorate found in the periods of crises. Hence, popular leaders turn out to be incompetent managers, while competent managers turn out to be uninspiring as leaders.

This is not an Italian problem - it is a European problem. And the most likely 'European solution' to it will be that Italians will have to vote again, relatively soon, like the Greeks almost a year ago, in a hope that forcing electorate to face 'explained' or rather 'better marketed' choices can yield the desired outcome, a la Ireland ca 12 June 2008 through 2 October 2009.

Subscribe to:

Posts (Atom)