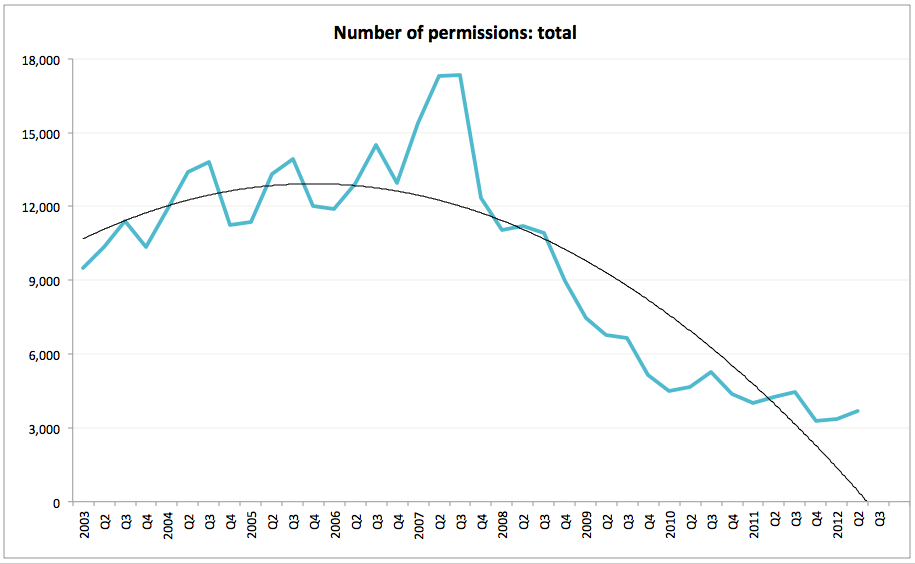

On foot of some comments to my earlier post on Ireland's migration flows, here are three charts to show in more details nationality breakdown of the core flows: Data refers to April-April data, so 2012 references period of April 2011 - April 2012.

Annual immigration:

- Total immigration peaked at 151,100 in 2007 and declined to the low point of 41,800 in 2010. Since then, it bounced somewhat back to 53,300 in 2011 and to 52,700 in 2012.

Annual emigration:

- Annual emigration hit bottom in 2006 at 36,000 and rose steadily to 49,200 in 2008. Thereafter, total emigration rose to 72,000 in 2009, dropped slightly to 69,200 in 2010 and shot up in 2011 (80,600) and 2012 (87,100).

Cumulated flows for 2006-2012:

- Cumulated net inflows for the period of 2006-2012 stood at 153,500 in April 2012.

- Irish nationals represent the only category of residents that registered net cumulated outflow (-23,400) in the period of 2006-2012.

- In 2006-2008, there were cumulated net inflows of 32,100 for Irish nationals and in 2009-2012 this was reversed to a cumulated net outflow of 55,500

- In 2006-2008, there were cumulated net inflows of 11,400 of UK nationals into Ireland, which was reversed to a cumulated net outflow of 2,300 in the 2009-2012 period

- In 2006-2008, there were cumulated net inflows of 14,100 for 'Rest of EU15' nationals and in 2009-2012 this was reversed to a cumulated net outflow of 5,800

- In 2006-2008, there were cumulated net inflows of 152,900 for EU12 nationals and in 2009-2012 this was reversed to a cumulated net outflow of 27,300

- In 2006-2008, there were cumulated net inflows of 30,600 for nationals from the rest of the world and in 2009-2012 there was a shallower net cumulated inflow of 3,600.