So, we have a new Presidential Pearl of Dumbness:

https://twitter.com/realDonaldTrump/status/1280209106826125313?s=20. I have compiled some earlier summaries of the same here: https://trueeconomics.blogspot.com/2020/05/2452020-trumpassery-of-coronavirus.html.

Accompanied by an academic institution's direct fact-checking:

And the actual facts, without the need for media interpreations:

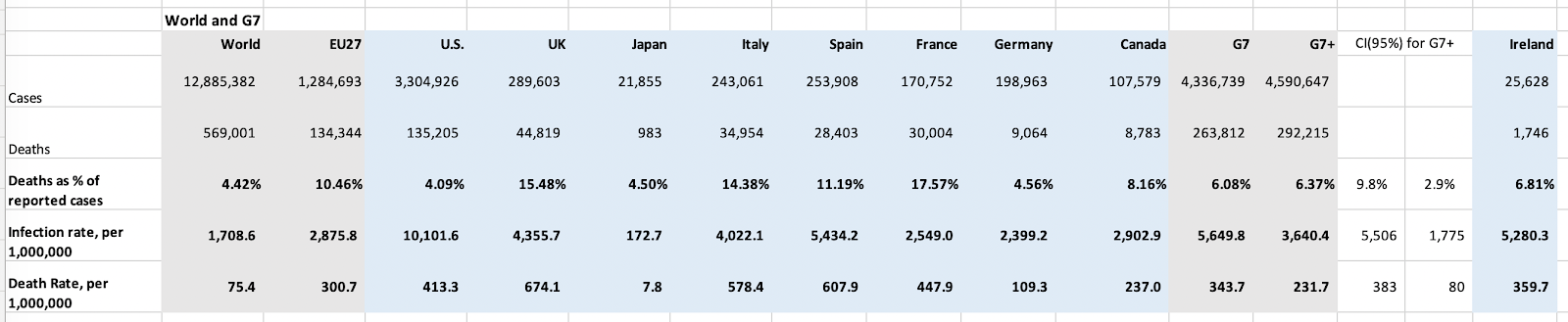

Why are we focusing on countries with > 25,000 cases as in above, instead on looking at global (every country) comparatives? Because COVID19 pandemic is the large numbers case. Countries with fewer cases, especially cases per capita, are experiencing much more volatile dynamics in daily data, which can easily skew comparatives.

So here are the descriptive stats for the group of 51 countries, plus EU27 as a whole, that provide some decent comparatives for the U.S.:

Q1: Is the U.S.'s 'case-fatality rate', or the number of deaths per 1,000 of reported cases, the lowest in the world?

A: No. Average case-fatality rate for 51 countries with highest number of total cases is 45.5. In the U.S. it is 44.34. Statistically, the U.S. is average in this metric. If we are to exclude the U.S. from the sample (to avoid 'double-counting') and exclude the UK and the EU27 - the set of countries with an earlier onset of the pandemic - the U.S. 'case-fatality rate' is above the average (36.5 is the upper bound for the confidence interval around the average). The U.S. 'case-fatality rate' ranks 20th highest in the group of 51 countries with more than 25,000 cases total.

Q2: Is U.S.'s death rate, or the number of deaths per 1 million of population, the lowest in the world?

A: No. Not by a mile. In fact, the U.S. death rate at 398.3 per 1 million is above the average for 51 countries (170.3) and above the upper boundary of the 95% confidence interval around the average (232.4). The U.S. death rate' ranks 7th highest in the group of 51 countries with more than 25,000 cases total.

So, Mr. President is shooting the proverbial verbal porkies once again... In fact, as the next post will show, the U.S. is a basket case when it comes to COVID19 outcomes even compared to the already basket case of the EU27. Alas, unlike the EU27, the U.S. does not have an excuse of being forced to deal with the pandemic in its earliest global development stages, when knowledge and better practices around the pandemic were not available to policymakers. Stay tuned...