Mortgages arrears data for private residences in Ireland for Q4 2012 was published today by the Central Bank of Ireland. Few surprises.

As expected, arrears rose. Unexpectedly, the rate of increase was much much slower than before in q/q terms and slower in y/y terms. As encouraging as this might sound, there are some points of concern outlined below. Here are some details of data dynamics first:

As expected, arrears rose. Unexpectedly, the rate of increase was much much slower than before in q/q terms and slower in y/y terms. As encouraging as this might sound, there are some points of concern outlined below. Here are some details of data dynamics first:

- In Q4 2012 there were a total of 792,096 accounts relating to private residential mortgages in Ireland - a massive y/y increase from 765,267 accounts in Q4 2011 due to 'reclassification' of some mortgages accounts.

- This 'reclassification' made historical comparatives in terms of, say, arrears as % of the total mortgages, utterly useless. This is how Irish official stats go: relabel, re-order, and if it makes things look better by coincidence - spin.

- Total number of mortgages in arrears for private residences rose from 141,389 accounts in Q3 2012 to 143,851 accounts in Q4 2012 - an increase q/q of 1.74%, well below any q/q increase since the beginning of the series. Average increase since Q3 2009 when the data started stands at 6.51%.

- Y/y total number of mortgages in arrears increased 21.43% in Q4 2012, the slowest rate of annual increases since the beginning of the series and below the average of 27.77%.

- Overall, in Q4 2012, 18.16% of all mortgages still outstanding in the country were in arrears. Adjusting for the CBofI 'reclassification' of mortgages accounts to allow for more direct historical comparative, 18.85% of all mortgages were in arrears.

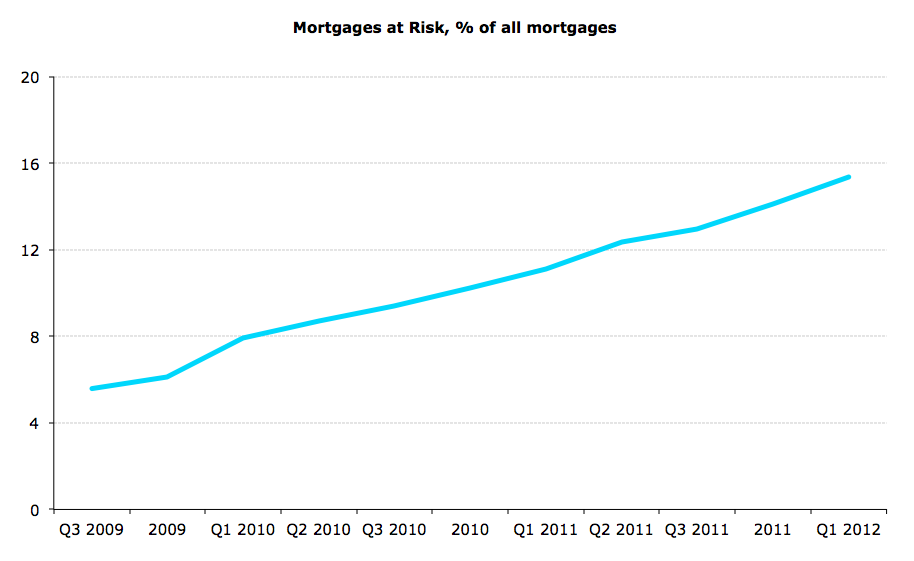

- Number of mortgages at risk or defaulted (defined as mortgages currently in arrears, restructured and not in arrears, plus repossessions) has risen in Q4 2012 to 186,785 (or 24.48% of the total adjusting for 'reclassifications', 23.58% based on official data) from 185,933 in Q3 2012. This implies a rise of 0.46% q/q and 19.61% y/y. Both represent the slowest rates of increase in series (short) history.

Two charts to illustrate:

Good news: the rates of arrears build up have slowed down in Q 2012.

Bad news, getting worse slower is not the same as getting better. Especially given the deterioration tallied from 2009 through today.

Worrying side: impacts of property taxes, banks guarantee lift-off, repossessions orders regime change, and personal insolvency 'reforms' are not visible in the current latest data. All represent a threat of accelerating arrears once again.

Real news: just under 1/4 of Irish private residences-linked mortgages are now at risk of default, in arreas or defaulted and some 650,000-700,000 people are currently impacted by this crisis to the point of being unable to meet the original conditions of their mortgages.