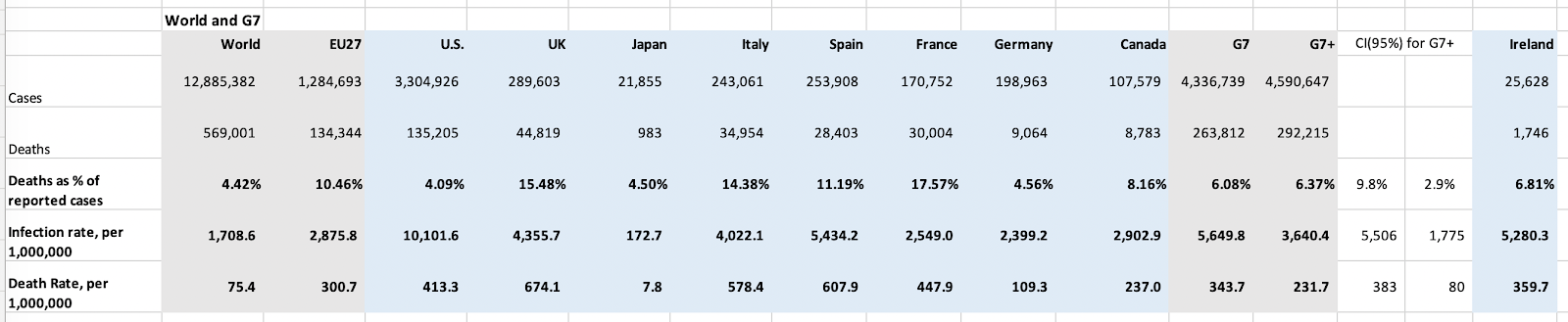

New data for the week prior on continued and new unemployment claims continues to support a view of a relatively slow and slowing-down recovery in the U.S. labour markets.

Continued unemployment claims:

Continued unemployment claims in the week of July 4 amounted to 17,338,000 down 422,000 on prior week. A week before, the rate of decline was 1,000,000, and in 4 weeks prior to the the week of July 4, 2020, average weekly rate of decline was 711,500. Current 4 weeks average rate of decline is 737,750 driven by two weeks of > 1 million declines. The good news is that we now have 8 consecutive weeks of drops in continued unemployment claims. The bad news is that we do not know how much of the decline from the COVID19 pandemic peak is down to benefits expirations, or due to benefits cancelations due to some income being earned, with restored income being below pre-COVID19 levels. In other words, we have no clue as to whether jobs being restored are of comparable quality to jobs lost.

Next, Initial Unemployment Claims: these remain troubling too. In the week of July 11, 2020, there were 1,503,892 new initial unemployment claims filed, the highest number in 5 weeks.

As the table above highlights, we now have more than 17 weeks of new unemployment claims filings in excess of 1 million. Note: new unemployment claims filings can reflect many factors, including:

- A person becoming newly unemployed;

- A person who was unemployed and temporarily left unemployment insurance coverage due to receipt of irregular earnings;

- A person who was unemployed, and run out of benefits coverage, taking a temporary job, but re-listing as an unemployed at that job expiration;

- A person who was unemployed before but did not secure past unemployment benefits; and

- A person who was unemployed but was denied prior benefits due to various reasons.

Here is the history of the Initial Unemployment Claims, smoothed out to a 3mo moving sum:

An updated employment outlook for July 2020: