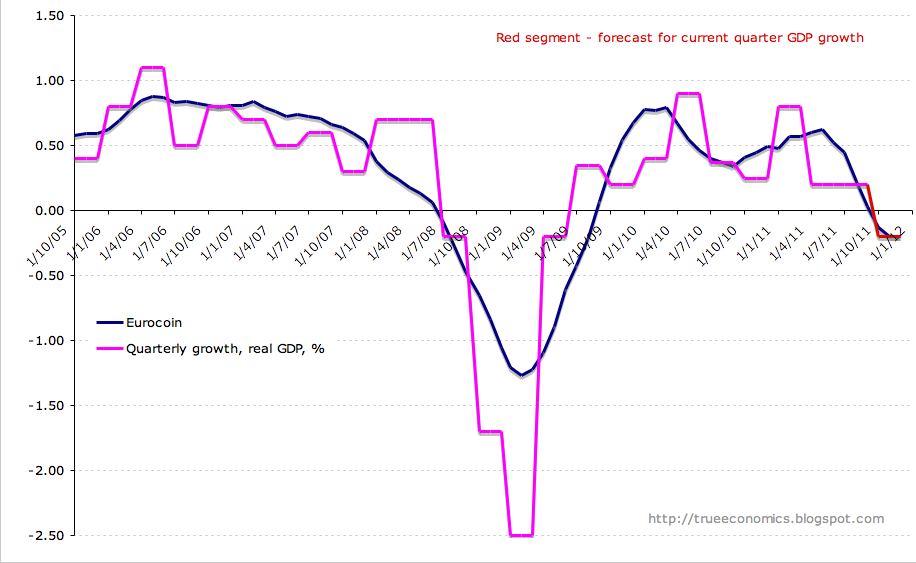

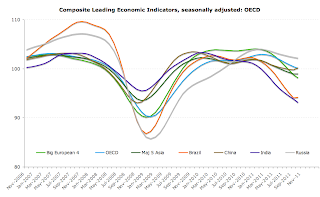

Latest leading economic indicators for Q4 2011 for OECD are not showing any real signs of economic recovery for the euro area. Here are some of the details (please note, data is through October, so forward signal is for November-December 2011).

For Australia, Q4 2011 indicator is now down at 100.55 against Q3 2011 reading of 100.80. 3mo MA is 100.71 against previous 3mo MA of 100.89. For comparative purposes, 2007 average reading was 101.96, 2009 average of 96.07 and 2010 average 101.13. 2011 average to-date is 100.99.

Canada's CLI is at 99.66, ahead of Q3 2011 reading of 99.42. 3mo MA is at 99.62 and previous 3mo MA was 100.72. 2011 average to-date is 100.90, well behind 102.13 average for 2010 and 101.26 average in 2007.

France current reading is at 98.13 slightly behind Q3 2011 at 98.60. 3mo MA is at 98.69, behind previous 3mo MA of 100.96. 2011-to-date average is at 101.16, behind 2010 average of 103.38 and 2007 average of 101.37.

Germany's current reading is at 98.28, down from 99.10 in Q3 2011 with current 3mo MA at 99.26, down from the previous 3mo MA of 102.93 - one of the highest rates of slowdown at 3.57%. 2011-to-date average is at 102.77, down from 2010 average of 104.08 and 2007 average of 103.96.

Ireland (for our local interest) is at 96.99 against Q3 2011 of 96.19 - one of the handful of countries (such as Greece) that shows some improvement. 3mo MA is at 100.40 against previous 3mo MA of 101.00. 2011-to-date reading is at 100.94 against 2010 average of 99.74 and 2007 average of 105.28.

Italy is currently reading at 96.55, down from 97.47 in Q3 2011. Current 3mo MA is at 97.50 down from 100.46 for previous 3mo MA - a decline of 2.95%. 2011-to-date average is 100.58 against 2010 average of 103.93 and 2007 average of 101.69.

Japan current reading is at 101.33 against previous reading of 101.55. 3mo MA at 101.62 down from 102.69 for previous 3mo MA. 2011-to-date average is 102.65 against 2010 average of 100.78 and 2007 average of 102.29.

Spain latest reading is 100.16 against previous reading of 100.65. 3mo MA is at 100.52 against previous 3mo MA of 101.18 and 2011-to-date average is at 101.38 against 2010 average of 102.86 and 2007 average of 102.52.

UK current reading is at 98.64 against previous reading of 99.01, with current 3mo MA of 99.14 against previous 3mo MA of 101.13 (-1.96%). 2011-to-date average is at 101.02 against 2010 average of 103.14 and 2007 average of 102.13.

US current reading is at 100.95 down from the previous reading of 101.25. 3mo MA is at 101.24, down from previous 3mo MA of 102.37 (-1.11%). 2011-to-date average is at 102.20 and 2010 average was 100.39, while 2007 average was 103.20.

In terms of EA17, current reading for the euro area stands at 98.53, down from previous reading of 99.13. 3mo MA currently stands at 99.20 against previous 3mo MA of 101.67 (down 2.43%). 2011-to-date average is at 101.75 against 2010 average of 103.34 and 2007 average of 102.81.

Big Euro Area 4 economies index is now at 98.12, down from the previous reading of 98.77. 3mo MA is at 98.88, down from 101.66 for the previous 3mo MA (-2.74%) and 2011-to-date average is at 101.66, down from 103.77 average for 2010 and 102.44 average for 2007.

Charts to illustrate:

For Australia, Q4 2011 indicator is now down at 100.55 against Q3 2011 reading of 100.80. 3mo MA is 100.71 against previous 3mo MA of 100.89. For comparative purposes, 2007 average reading was 101.96, 2009 average of 96.07 and 2010 average 101.13. 2011 average to-date is 100.99.

Canada's CLI is at 99.66, ahead of Q3 2011 reading of 99.42. 3mo MA is at 99.62 and previous 3mo MA was 100.72. 2011 average to-date is 100.90, well behind 102.13 average for 2010 and 101.26 average in 2007.

France current reading is at 98.13 slightly behind Q3 2011 at 98.60. 3mo MA is at 98.69, behind previous 3mo MA of 100.96. 2011-to-date average is at 101.16, behind 2010 average of 103.38 and 2007 average of 101.37.

Germany's current reading is at 98.28, down from 99.10 in Q3 2011 with current 3mo MA at 99.26, down from the previous 3mo MA of 102.93 - one of the highest rates of slowdown at 3.57%. 2011-to-date average is at 102.77, down from 2010 average of 104.08 and 2007 average of 103.96.

Ireland (for our local interest) is at 96.99 against Q3 2011 of 96.19 - one of the handful of countries (such as Greece) that shows some improvement. 3mo MA is at 100.40 against previous 3mo MA of 101.00. 2011-to-date reading is at 100.94 against 2010 average of 99.74 and 2007 average of 105.28.

Italy is currently reading at 96.55, down from 97.47 in Q3 2011. Current 3mo MA is at 97.50 down from 100.46 for previous 3mo MA - a decline of 2.95%. 2011-to-date average is 100.58 against 2010 average of 103.93 and 2007 average of 101.69.

Japan current reading is at 101.33 against previous reading of 101.55. 3mo MA at 101.62 down from 102.69 for previous 3mo MA. 2011-to-date average is 102.65 against 2010 average of 100.78 and 2007 average of 102.29.

Spain latest reading is 100.16 against previous reading of 100.65. 3mo MA is at 100.52 against previous 3mo MA of 101.18 and 2011-to-date average is at 101.38 against 2010 average of 102.86 and 2007 average of 102.52.

UK current reading is at 98.64 against previous reading of 99.01, with current 3mo MA of 99.14 against previous 3mo MA of 101.13 (-1.96%). 2011-to-date average is at 101.02 against 2010 average of 103.14 and 2007 average of 102.13.

US current reading is at 100.95 down from the previous reading of 101.25. 3mo MA is at 101.24, down from previous 3mo MA of 102.37 (-1.11%). 2011-to-date average is at 102.20 and 2010 average was 100.39, while 2007 average was 103.20.

In terms of EA17, current reading for the euro area stands at 98.53, down from previous reading of 99.13. 3mo MA currently stands at 99.20 against previous 3mo MA of 101.67 (down 2.43%). 2011-to-date average is at 101.75 against 2010 average of 103.34 and 2007 average of 102.81.

Big Euro Area 4 economies index is now at 98.12, down from the previous reading of 98.77. 3mo MA is at 98.88, down from 101.66 for the previous 3mo MA (-2.74%) and 2011-to-date average is at 101.66, down from 103.77 average for 2010 and 102.44 average for 2007.

Charts to illustrate: