Why cryptos might not prevail? Because of this:

Or, put differently, because the entire hype around cryptocurrencies, and increasing also blockchain technology, is based on myths.

Let's tackle the above, shall we?

Are cryptos a liquid market? No. In fact, the markets are illiquid (see here:

http://trueeconomics.blogspot.com/2017/12/81217-coinbase-to-bitcoin-flippers-you.html) and worse, transactions costs for even basic movement of Bitcoin across accounts are atrocious today (in markets without a direct liquidity squeeze, amounting, sometimes to 15%). See

https://www.bloomberg.com/view/articles/2017-11-14/bitcoin-s-high-transaction-fees-show-its-limits and

https://www.bloomberg.com/news/articles/2017-09-29/paying-15-to-send-25-has-bitcoin-users-rethinking-practicality. Imagine what these can balloon to in a liquidity squeeze event. And then there is concentration issue:

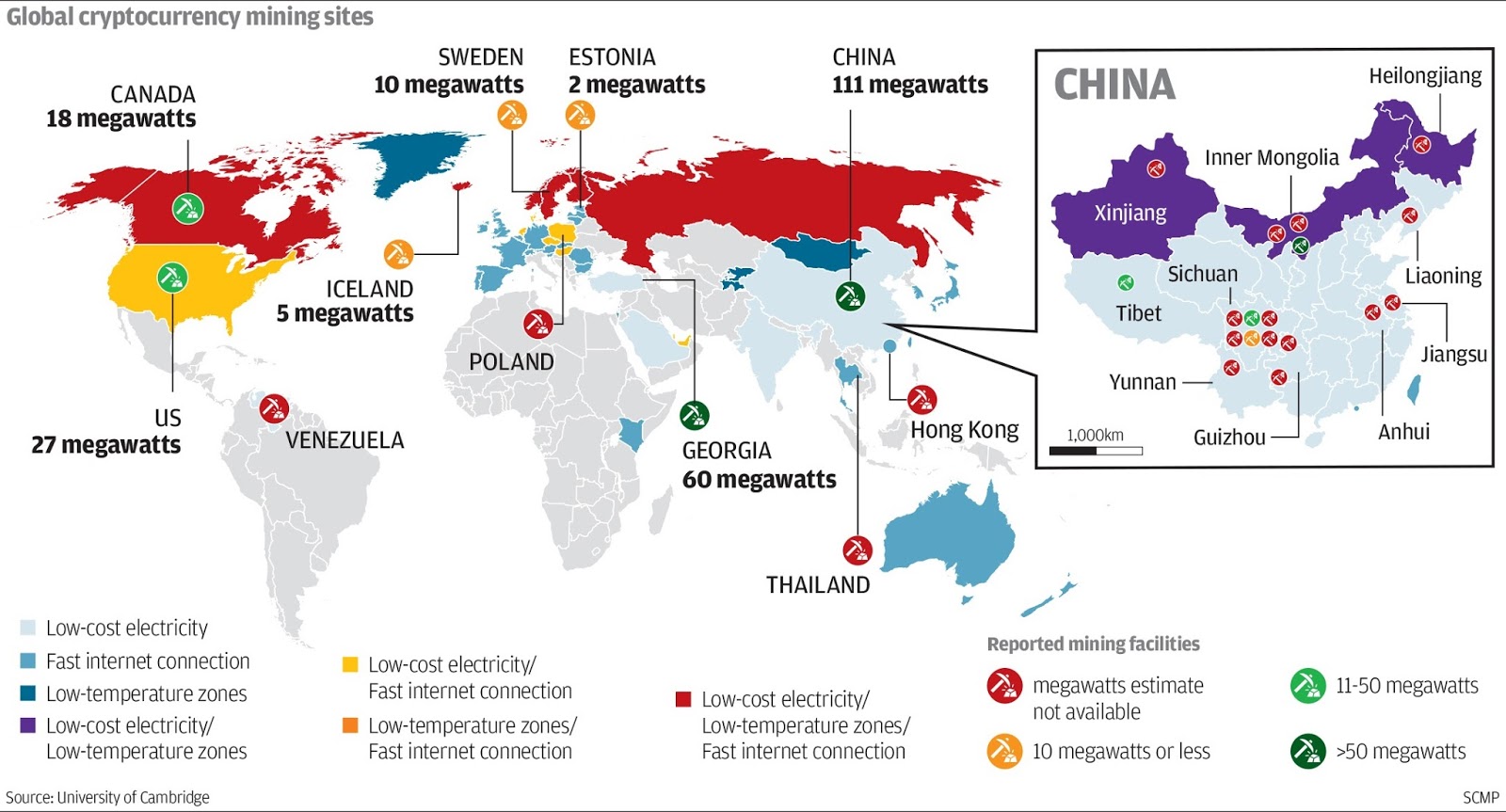

http://www.zerohedge.com/news/2017-12-08/bulgaria-government-shocked-discover-it-owns-3-billion-bitcoin and the 1,000 'whales' problem. Oh, no, these are

not liquid markets.

Are cryptos global? Yes, if you consider Venezuela, China, Japan and other places where either hype or regulatory evasion or hyperinflation are driving demand for BTC. Yes, if you consider markets for illicit funds flows to be global. No, if you consider usability of BTC in standard sense of money (as a medium of exchange). See

https://www.bloomberg.com/gadfly/articles/2017-12-01/bitcoin-is-hot-until-you-actually-try-to-spend-some. It turns out that as a medium of exchange (one function of money) it is utterly useless. It is also useless as a unit of accounting, which is another function of money (no one accepts 'bitcoin-priced accounts' and its volatility makes any attempt at preparing bitcoin-based accounts futile). And bitcoin is horror who as a store of wealth (third function of money), because so far, it has a combination of sky-high volatility, positive correlation with interest rates and upward trend, while also having sky-high volatility to the downside, which suggests that any trend reversal will be really ugly. Now, you do not store wealth over one month (as arguments in favour of bitcoin go), but you store it over the years. And here, bitcoin is untested at best, recklessly dangerous at worst. Take you 'happy middle' pick.

Are cryptos less susceptible to corruption? You need your head examined to believe in this: cryptos are subject to waves and rounds of pump-and-dump scams, potential insider theft, and insider hacks. Worse, they are clearly being used (at least to some extent) to sustain illicit trade and finance flows, and to launder money. Cryptos 'whales' can collude at any point in time to fix the markets in their favour. If bitcoin is susceptible to corruption, a free-for-all unregulated bazar crossed with the Silk Road would be a 'well functioning exchange'.

Possibility of a fractional ownership is clearly available to bitcoin 'investors'. No doubt. So is possibility of fractional ownership for those buying elephants as pets or condos in Bahamas. Hell, you can even have a fractional ownership of a few acres on the Moon. End of story.

Highly secure networks are

not a feature of cryptocurrencies, as we all know. Frequency of hacks and other cyber events involving cryptos exchanges this year

exceeds the same for large corporate IT infrastructures, according to our research data. Put differently, cryptos appear to be more frequently targeted by cyber crime and/or are more vulnerable to attacks and theft than larger publicly listed corporations. Now, notice that, for now, vulnerability is in wallets and exchanges,

not in blockchain itself. 'For now' is the key bit. We do know that cybercriminals are incentivised by abnormally high returns to crime (see

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3033950) and we know that cybercrime is evolving rapidly to acquire ever-expanding capabilities, tools and strategies. It is simply inconceivable that blockchain will remain 'unhackable' into the near future. More importantly, current evidence of the lack of efficient corruption of the blockchain itself rests on the assumption that it is technology that is a barrier to entry for the cyber criminals. This is an untested proposition. In reality, most likely, the reason for lack of efficient penetrations into blockchain system itself is the existence of the low-hanging fruit in the form of exchanges and wallets, as opposed to the impenetrability/security of the blockchain itself.

Blockchain 'changing incentives structure' is the daftest argument in favour of anything, including the blockchain. There is no 'incentives structure' difference between holding/investing in a BTC and holding/investing in any other speculative asset. None. Full stop. Bitcoiners and blockchainers

did not change human nature. They

did not rewrite our positive and negative incentives systems. To claim otherwise is to impose such a vast range of assumptions on our behavioural incentives and constraints as to make basic economics 101 sound like a reality-hugging discipline of empirical rigour.

'Code wins against theory' is another 'incentives change' mumbo-jumbo. Code, in the case of Bitcoin and cryptos,

is theory. Not because it is physically disembodied from the currency. But because it is the basis for the key assumption (axiomatic theory, idiots?) of 'trust'. Bitcoiners are quick to point that there is no 'mistrusted' Central Banker behind the BTC, because there is a 'trusted mathematical algo' behind it. I rest my point, folks. Because you know 'trusted' and 'mistrusted' terms are (1) the defining terms of the bitcoiners' logic, and (2) these terms have nothing to do with logic or mathematics: they are purely subjective. 'Code

is theory', morons, because it only matters as long as we believe it matters.

Do bitcoin or cryptos remove 'systems inefficiencies'? Doh! See transactions costs above, lack of exchange medium function, above, lack of storage and exchange security, above. The promise of the blockchain is to reduce systems inefficiencies when it comes to registering and storing information. This has nothing, repeat, nothing to do with BTC or cryptocurrencies. Besides that, there is a host of major problems with market efficiency of bitcoin (see

https://www.forbes.com/sites/francescoppola/2017/07/26/the-fundamental-conflict-at-the-heart-of-bitcoin/2/#527d30435aac and

https://arxiv.org/abs/1704.01414). In basic terms, today, Visa and Mastercard are vastly more efficient (in cost, time and security of transactions sense) than BTC is. Worse, as bitcoin rage evolves, efficiencies of the crypto to act as an information clearing platform are further reduced by system congestion. If anything, the boom we are witnessing is 'creating inefficiencies' rather than reducing them.

Finally, there is the last argument that 'enough talented people believe' in cryptocurrencies to warrant their rise to power. Oh, dear. Enough talented people believed in the property bubble, in the dot.com bubble, in

every bubble, to drive the respective assets to mad levels of valuations and the eventual crashes. Enough talented people believed that the Sun revolves around the Earth at some point in time too. Talented people beliefs are not exactly a decent test for resilience or sustainability or success of anything. Let alone, cryptos. Why 'let alone'? Because in cryptos case, 'enough talented people' pool of believers is a highly skewed pool of 'talent' defined by affinity for one type of technology. In a way, 'enough talented people' here is equivalent to the Church of Scientology. They define their own breed of 'talented people' by identifying them as believers in the Church. It is a circular argument, folks.

So, no, none of the above arguments are either necessary or sufficient to establish the future of cryptocurrencies or the BTC. Try again. Try harder.