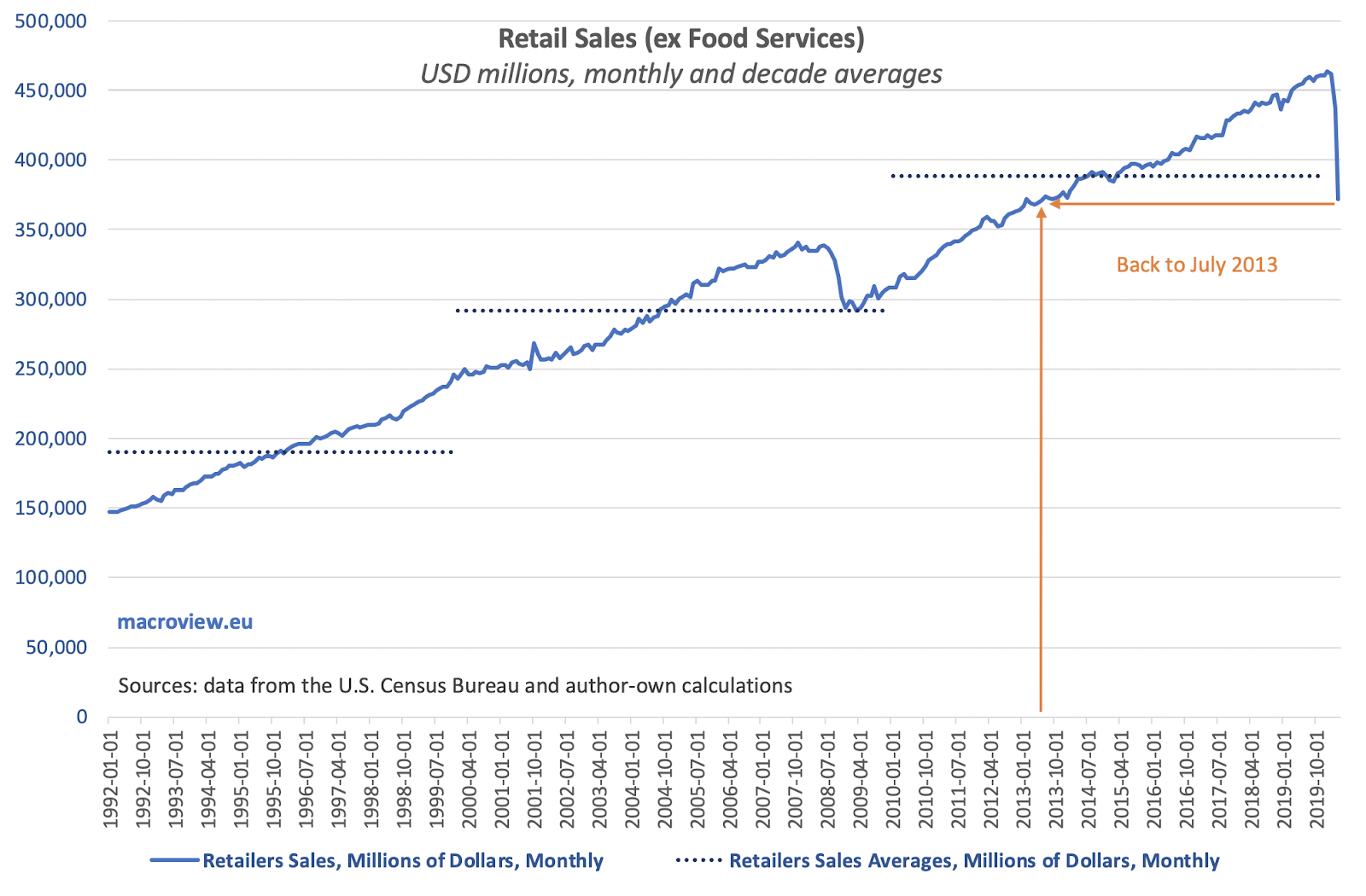

For those of you following this blog this would be a familiar sight: I have been worrying about the underlying structure of the U.S. labor markets for some time now. The ongoing recovery appears to be relatively robust in terms of headline figures, e.g. GDP growth rates and declining continued unemployment claims. But in reality, it has been nothing but the return to trends that persisted before the pandemic - trends that are extremely worrying.

I covered the fact that longer term unemployment has now gone through the roof: https://trueeconomics.blogspot.com/2021/04/14421-share-of-those-in-unemployment-27.html. And beyond this, there is a bigger problem of historically low levels of labor force participation. We are witnessing a massive pull-away within the skills distribution in the U.S. economy: there are shortages of skilled labor, including in manufacturing, and there is massive outflow of people from the labor markets in lower skills groups.

Just look at the absolute disaster of the 'recovery' when it comes to people who have left the workforce alltogether:

If you think this is a 'robust' recovery, you really need to think a bit harder: we are having a secular stagnation in the female labor force and we are having a long term depression in the male labor force. And these trends are not subject to demographics of aging.