Updating the Residential Property Price Index data from CSO released earlier this week, here are the core highlights for September 2013:

For Houses RPPI:

Dublin RPPI:

- All country RPPI rose to 68.2 in September from 67 in August, marking sixth consecutive month of rises The index is now up 3.65% y/y (in August it was up 2.76% y/y).

- 3mo cumulated change in RPPI is 3.96% and 6mo cumulated change is 6.4%. 6mo average rise is 0.66%.

- Nama valuations (with 10% cushion on LTEV uplift and risk sharing) are now 33.97% off the mark.

- Relative to peak, index now stands at -47.74% and relative to absolute minimum it is at +6.4%.

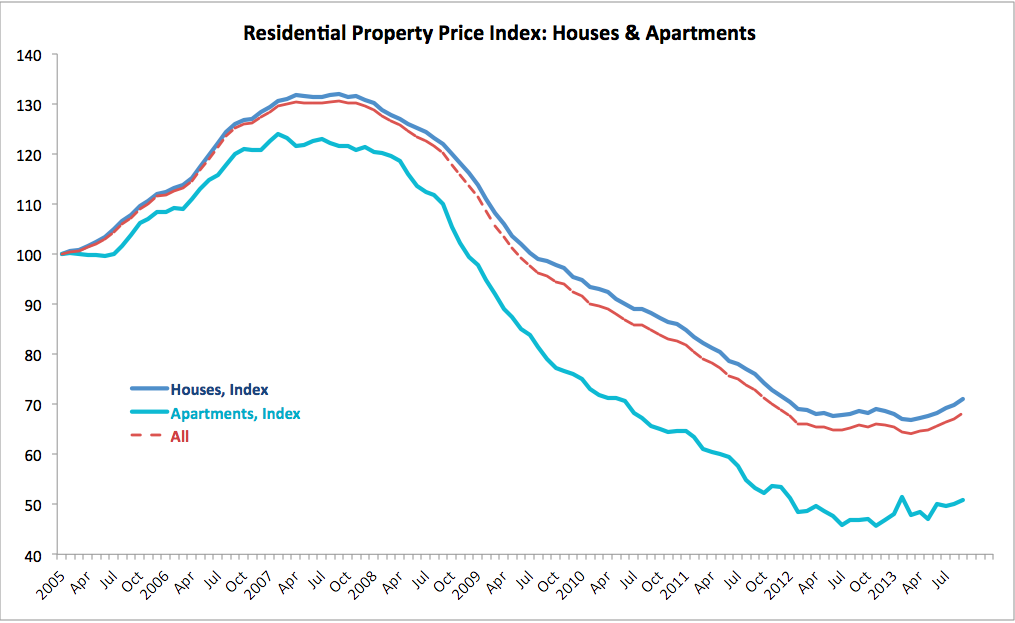

For Houses RPPI:

- Index rose to 71.0 in September from 69.8 in August and posted a 3.35% rise y/y.

- 3mo cumulated gains are at 4.11% and 6mo cumulated gains are at 6.29%. Average over 6 months monthly increase is 0.69%.

- Relative to peak, the index now stands at -46.21% and relative to absolute minimum it is at +6.29%.

- September marked sixth consecutive month of rises in house prices.

For Apartments:

- Index rose to 50.9 in September from 50.0 in August and posted a 8.53% rise y/y.

- 3mo cumulated gains are at 1.6% and 6mo cumulated gains are at 6.26%. Average over 6 months monthly decrease is -0.41%.

- Relative to peak, the index now stands at -58.92% and relative to absolute minimum it is at +11.38%.

- September marked second consecutive month of rises in apartments prices.

Dublin RPPI:

- Index rose to 65.9 in September from 63.4 in August and posted a massive 12.27% rise y/y.

- 3mo cumulated gains are at 9.47% and 6mo cumulated gains are at 12.07%. Average over 6 months monthly increase is 1.13%.

- Relative to peak, the index now stands at -51.0% and relative to absolute minimum it is at +15.01%.

- September marked sixth consecutive month of rises in Dublin property prices.

Conclusions:

- Twin convergence toward long-term equilibrium prices is now evident in Dublin markets (upward price pressures) and National ex-Dublin prices (downward pressures).

- The core question is when will Dublin prices overshoot their long-run trend and moderate again?

- Another core question is what the fundamentals determined price levels are for Dublin and for the rest of the country?

- I have no answers to the above questions and anyone who says they do is most likely talking porkies.

- What I do know is that there are plenty of risks to the downside and headwinds working through the economy. These include: mortgages arrears, income effects of tax and charges changes in Budget 2014, banks rates on existent mortgages; and new mortgages supply and pricing.

- So far, my gut feeling is that we are still on a sustainable upward trend in Dublin and on moderating negative trend in the rest of the country.

I make a similar poitn in this blog, would appreciate your feedback

ReplyDeletehttp://irishpropertytax.blogspot.co.uk/2013/10/the-south-dublin-property-bubble-storm.html

This comment has been removed by the author.

ReplyDeleteI believe we have a dead cat bounce in Dublin. Don't buy, the downside risks are substantial.

ReplyDeleteTo Anonymous. I am not sure - we have a relatively sustained (6mo) uplift. And overall, gentle upward trending for some 15-18 months now. Not exactly consistent with a 'dead cat bounce'. That said, as I pointed out - headwinds are huge.

ReplyDeleteCall a number of Estate Agents throughout South County Dublin and they will confirm that the recent price increases ceased very abruptly about 3-4 weeks ago.

ReplyDeleteRises in 2012 & 2013 were cash-buyer driven.

It takes a long time to build up the finances to become a cash buyer.

Consequently, the replenishment rate is low.

With each cash buyer purchase, this group shrinks in size.

You then become more reliant on bank finance to sustain price increases.

Currently, the banks do not have the capital/lending power to take up the slack.

Now add into the mix forthcoming repossessions and new builds/completions.

Only yesterday it was reported there are 120,754 mortgages in arrears.

There is an extreme (and artificial) lack of supply in the market which has fueled the price increases.

As supply begins to kick in, I would expect it to have a further dampening effect on prices.

All things being considered, this is looking more and more like a dead cat bounce.