This is an unedited, longer, version of my article for the Sunday Business Post covering my outlook for oil prices.

Traditionally, crude oil acts as a hedge and a safe haven against currencies and bond markets volatility. Not surprisingly, during the upheaval of the U.S. Presidential election this week, when dollar went into a temporary tailspin, equity markets sharply contracted and bonds prices fell, all eyes turned to the risk management staples: gold, oil and, on a more exotic side of trades, Bitcoin. Gold and Bitcoin did not surprise, staunchly resisting markets sell-offs and gaining in value. But oil prices tanked. The old, historically well-established correlation did not apply. Instead of rising, U.S. oil futures fell in the immediate aftermath of Donald Trump’s surprise victory, and then, in line with the stock markets, futures rose. Within the day, U.S. crude futures prices were back at USD45.27 a barrel on the New York Mercantile Exchange, while Brent rose back USD46.36 marker. More broadly, the S&P 500 Energy Sector Index rose 1.5 percent within 12 hours of the election results announcement.

This breakdown in historical patterns of correlations between crude and financial assets prices underlines the simple reality of the continuous oil markets slump: we are in the new normal of systemically low oil valuations underpinned by the very same driving forces that precipitated the crude price collapse from over USD100 per barrel to their mid-to-high 40’s today. These forces are three-fold, comprising reduced demand for energy, reduced demand for oil as a source of energy, and increased supply of oil.

Prices and Stocks

Currently, oil prices are rebounding from the eight-week lows, but prices remain sensitive to any signals of changes in demand and supply. The reason for this is the excess stockpile of oil stored in tankers, ground facilities and at refineries. Most recent U.S. federal data showed oil stockpiles swelling well ahead of the markets expectations, as producers continue to pump oil unabated.

U.S.-held inventories of oil were at 2.43 million barrels at the beginning of November, based on the data from the U.S. Energy Information Administration. American Petroleum Institute puts total stocks of oil in storage and production at 4.4 million barrels - more than 1 million barrels in excess of the seasonally-adjusted forecast for demand. And at the end of October, the U.S. posted a 34-year record in weekly increases in crude and gasoline stocks - at 14.4 million barrels.

The U.S. is no exception to the trend. OPEC recently revised its outlook for oil price recovery for the next three years based on the cartel’s expectation that current levels of production will remain in place for longer than anyone anticipated. Per OPEC latest forecast, we won’t see oil hitting USD60 per barrel until 2020. Only twelve months ago, OPEC forecast for 2020 was USD80 per barrel.

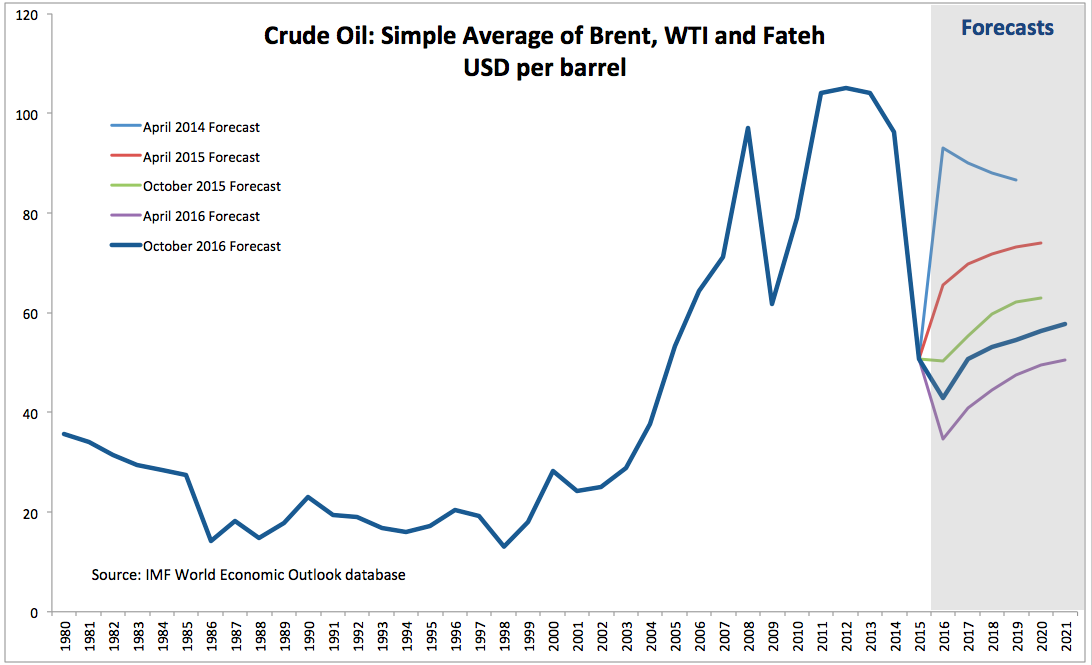

Similar forecasts revisions were produced a month ago by the IMF. In its World Economic Outlook forecast, the IMF revised its outlook for 2016 crude prices from USD50.54 per barrel forecast in October 2015 to USD 42.96 per barrel. 2017 full year price forecast moved from USD55.42 in October 2015 to USD50.64 in October 2016. If in 2015 the IMF was predicting oil prices to hit USD60 marker by mid-2018, today the Fund is projecting oil prices remaining below USD58 per barrel through 2021.

Both, the OPEC and the IMF forecast lower global economic in 2016 and 2017. The IMF outlook is based on world GDP expanding by just 3.08 percent in 2016 and 3.4 percent in 2017, well below post-Crisis average of 3.85 percent and pre-crisis average of 4.94 percent. OPEC forecast for oil prices is based on similarly pessimistic growth outlook for 3.4 percent average growth over the next six years, down from 3.6 percent forecast issued in October 2015.

Alternative Energy: Rising Substitutes

As demand for energy in general remains weak, alternative sources of energy are starting to take a larger bite out of the total energy consumption. Solar power capacity has almost tripled in the U.S. over the last 3 years. Renewables share of the U.S. power supply rose from around 4 percent of total power generation in 2013 to 8 percent this year, on its way to exceed 9 percent in 2017. Solar energy supply is now growing at a rate of almost 40 per annum, spurred on by the Federal solar tax credits, extended by the Congress in early 2016. In Germany, following the Government adoption of Energiewende policies — a strategy that aims to move energy supply away from oil and uranium — renewables now provide almost 30 percent of electricity, on average. And Gwermany’s upper chamber of parliament, the Bundesrat, has passed a resolution calling on the EU to create a system of harmonised taxation and vehicle duties that can ensure that only emission-free cars will be registered in Europe by 2030. On the other side of the spectrum, in the OPEC member states and Russia, renewables energy production is currently standing at below 5 percent of total energy demand. While the number is relatively low, it is rising fast and countries from Saudi Arabia to United Arab Emirates to Russia - all have significant ambitions in terms of lifting non-oil based energy output. In Abu-Dhabi, a recently approved solar energy project will deliver electricity at a cost below coal-fired power plants, at 2.42 US cents per kilowatt-hour, setting world record for the cheapest solar energy supply. Dubai plans to get 25 percent of its energy needs from renewables by 2030. The target is to reach 75 percent by 2050. Even Iran is opening up to use of renewables, with wind and solar investments in 2016-2017 pipeline amounting to close to USD12 billion. In Jordan, just one wind farm - a 38-turbine strong Tafila - is supplying 3 percent of country electricity, since production began in 2015.

All-in, globally, estimated 7 percent of oil demand decline over the last 5 years is accounted for by energy sources substitution. The key drivers for this trend are new environmental agreements, putting more emphasis on alternative energy generation, local environmental pressures (especially in China), and the desire to shift oil production to export markets, away from domestic consumption. Another incentive is to use clean power to reduce domestic subsidies to fossil fuels. According to the IMF report published earlier this year, Middle East, North Africa and Central Asia account for almost one half of the total worldwide energy subsidies. Since the onset of the oil price shock, UAE, Egypt, Oman and Saudi Arabia have been cutting back on fossil fuels subsidies and bringing retail prices for energy closer to market standards.

The second order effect of the above changes in energy composition mix is that moving away from subsidised fossil fuels improves markets transparency and reduces corruption. It also compensates for declines in oil prices in terms of exports earnings.

Drilling at These Prices?

As slower global growth and increasing substitution away from fossil fuels are suppressing demand for oil, supply of the ‘black gold’ is showing no signs of abating. Per latest OPEC statement, oil producers, especially in North America, surprised markets analysts by failing to curb production volumes in response to weak prices. OPEC members have been running production volumes near historical records through out the 3Q 2016. And in the U.S., the Energy Department raised its production forecasts for both 2016 and 2017. However, U.S. crude output this year is unlikely to match the 2015 levels - the highest on record since 1972. All in, the Energy Department now estimates that 2016 average daily production will be around 8.8 million barrel per day (bpd), which is lower than 9.5 million bpd delivered in 2015, but more than forecast for 2016 back in September. Likewise, for 2017, the Energy Department revised its September forecast from 8.57 million bpd to just over 8.7 million bpd in October. Through the second and third quarters of 2016, North American drillers actually increased drilling activity as prices improved relative to late 2015. The number of active oil rigs operating in the U.S. is now up by more than 130 compared to May counts and the rate of new rigs additions is remaining high, rising to 2 percent last week alone.

Russia and Iran

A combination of stagnant or even declining demand, and expanding production means that the only change in the flat trend in oil prices over the next 6-12 months can come only from a policy shock on the supply side. For OPEC, Iran and Russia such a shock is unlikely to happen. Majority of oil exporting economies have either fully (as in the case of Russia and Iran) or partially (as in the case of Saudi Arabia) adjusted their economic policy frameworks to reflect low price of energy environment.

I asked, recently, Konstantin Bochkarev of Forex-BKS, who is one of the leading financial markets analysts working in the Russian markets for a comment on the current state of play in Russian economic policies in relation to oil prices. In his view, “It looks like the worst is over for the Russian economy in terms of adaptations to low oil prices, Western sanctions, geopolitical risks and other challenges of last two years. Sub-50-55 USD oil or even $40 is the new reality and it doesn’t scare any more. On the other hand low efficiency of the economic policy in Russia (due to a lot of constraints like the lack of reforms and the will to change anything before the President election in 2018) means that there’s rather huge cap for the Russian GDP growth which can be limited by 1%-1.5% at 40-55 USD oil.” Overall, “the «crisis policy» which was rather successful during this recession and led to the stabilization of the macroeconomic situations. The recapitalization of the Russian banking system, free float of the Russian ruble, higher interest rates, the transparency of the CBR policy and rather tight budget policy. All these measures finally led to 6% inflation by the end of 2016, rather sufficient decrease in volatility of the Russian ruble and less correlation with oil prices.” And moving away from the petroleum-dominated economy has had even deeper impact. Per Bochkarev, “Oil can’t solve all your problems any more whether it’s 40$ or 100$, because changing social and business environment, external and internal challenges demand something more than budget without deficit or stable cash flow. Still low oil prices can accelerate changes in the Russian economy and society and lead to some necessary reforms or unpopular measures.”

In a sense, Russian experience shows the direction that many oil exporting economies are heading in the age of low oil prices: the direction of accelerated fiscal and monetary responses and gradual structural economic reforms. In some areas, Russia took its medicine first and in a larger dose, but other big producers, including Iran and Saudi Arabia, as well as UAE are also traveling down the same path.

As an aside, it is worth noting that Iranian production is growing ahead of expectations. Per Bloomberg report: “Output at the fields west of the Karoun River, near Iran’s border with Iraq, rose to about 250,000 barrels per day from 65,000 barrels in 2013, the Oil Ministry’s news service Shana reported Sunday, citing President Hassan Rouhani at a ceremony to formally open the project. Iran had expected to reach that output target by the end of the year, Mohsen Ghamsari, director for international affairs at the National Iranian Oil Co., said in September.” (http://www.bloomberg.com/news/articles/2016-11-13/iran-pumps-more-oil-as-saudi-minister-calls-for-opec-output-cuts)

Since the easing of the sanctions, starting with end of January 2016, Iran’s output rose from just around 2.82 million bpd to ca 3.65 million bpd.

Russian producers are also hardly feeling a pinch. According to Bochkarev, “Tax system plays a much more important role in the Russian oil companies production decisions than the rise or fall in oil prices. Whether oil is $40 or $100 per barrel majors are generating generally the same financial results. Besides almost oil majors are stable even at $30 oil. The decreases in oil prices are easily compensated by the fall in the ruble exchange rate. So cost control or cost cutting plays much more important role in other sectors of the Russian economy.”

Still, Russia and Iran might be heading into a direct competition in the European markets, where geopolitics and legacy contracts are changing the playing field away from simple price competition. This new - since January 2016 - competitive dynamic may be a longer term, rather than a current issue, however, according to Bochkarev. “It doesn’t look like that Iranian oil is huge challenge for Russian majors next several years. Numerous consumers who stopped buying the oil from Iran due to sanctions made some changes to their refinery or productions lines and equipment. So Iran has to offer some kind of bonus or lower oil prices to make them return to its oil. Probably it’s much easier for Iran to deal with China, India and other countries in Asia in order to find export markets for its oil. Iran can try to restore market share in Europe but the other hand of such policy can be lower oil prices or necessary discounts. LNG Imports from the US as well as the bigger role of Qatar and Iran in the future are already evident in European markets. The unique status of Gazprom is probably now a matter of the past but the more competitive market can finally make Gazprom more competitive.”

Trump Cards

Which means that economic policies shocks that can alter the current flat growth trend for oil prices are unlikely to come from the OPEC+ countries. Instead, the key to the near-term future variation in oil price trend will most likely come from the U.S. The markets are still assessing the full impact of Mr. Trump’s victory on his foreign and energy policies - the two key areas that are likely to alter the supply side of oil equation, as well as his economic policies that might influence the demand side and inflation. Starting with the latter, if - as promised during the election - the new White House Administration deploys a significant infrastructure and spending stimulus across the U.S. economy, we can expect both the demand for oil to firm up, clearing out some, but not all of the excess supply currently available in the markets. A stimulus to the U.S. growth is also likely to trigger higher inflation. With oil generally being a historical hedge against inflationary pressures, the likely outcome of improved growth performance across the U.S. will be a rise in oil prices from the current range of mid-40s to mid-50s and upper-50s, slightly above the IMF forecasts for 2017 and well ahead of the current market prices.

On the other hand, President-elect has promised to shift Federal supports away from alternative energy toward ‘clean coal’, oil and gas sectors. If he gets his way, the impact will be more American oil flowing to exports and higher excess supply, with lower prices. Mr. Trump’s election is likely to see the Republicans-controlled Congress moving to approve more export-driven pipelines, reducing the cost of oil transport from shale oil rich regions, such as Ohio and Pennsylvania, as well as North Dakota, and increasing incentives to boost production levels. Beyond stimulating production of the U.S. oil, Trump Administration is also likely to green light Keystone XL pipeline that will connect Canadian oil sands to exports terminals in the Gulf of Mexico. This will further expand supply of cheaper oil in the global markets.

Combining the two factors, it appears that the current IMF and OPEC outlook for 2017 for oil prices may be rather optimistic.

Barring a significant surge in global (as opposed to the U.S. alone) growth, and absent supportive cuts to production by the OPEC and other major producing countries, in all likelihood we will see oil prices drifting toward USD52-55 per barrel range toward the second half of 2017. Until then, any significant repricing of oil from USD47-48 per barrel price levels up will be a speculative bet on strong economic growth uptick in the U.S.

Traditionally, crude oil acts as a hedge and a safe haven against currencies and bond markets volatility. Not surprisingly, during the upheaval of the U.S. Presidential election this week, when dollar went into a temporary tailspin, equity markets sharply contracted and bonds prices fell, all eyes turned to the risk management staples: gold, oil and, on a more exotic side of trades, Bitcoin. Gold and Bitcoin did not surprise, staunchly resisting markets sell-offs and gaining in value. But oil prices tanked. The old, historically well-established correlation did not apply. Instead of rising, U.S. oil futures fell in the immediate aftermath of Donald Trump’s surprise victory, and then, in line with the stock markets, futures rose. Within the day, U.S. crude futures prices were back at USD45.27 a barrel on the New York Mercantile Exchange, while Brent rose back USD46.36 marker. More broadly, the S&P 500 Energy Sector Index rose 1.5 percent within 12 hours of the election results announcement.

This breakdown in historical patterns of correlations between crude and financial assets prices underlines the simple reality of the continuous oil markets slump: we are in the new normal of systemically low oil valuations underpinned by the very same driving forces that precipitated the crude price collapse from over USD100 per barrel to their mid-to-high 40’s today. These forces are three-fold, comprising reduced demand for energy, reduced demand for oil as a source of energy, and increased supply of oil.

Prices and Stocks

Currently, oil prices are rebounding from the eight-week lows, but prices remain sensitive to any signals of changes in demand and supply. The reason for this is the excess stockpile of oil stored in tankers, ground facilities and at refineries. Most recent U.S. federal data showed oil stockpiles swelling well ahead of the markets expectations, as producers continue to pump oil unabated.

U.S.-held inventories of oil were at 2.43 million barrels at the beginning of November, based on the data from the U.S. Energy Information Administration. American Petroleum Institute puts total stocks of oil in storage and production at 4.4 million barrels - more than 1 million barrels in excess of the seasonally-adjusted forecast for demand. And at the end of October, the U.S. posted a 34-year record in weekly increases in crude and gasoline stocks - at 14.4 million barrels.

The U.S. is no exception to the trend. OPEC recently revised its outlook for oil price recovery for the next three years based on the cartel’s expectation that current levels of production will remain in place for longer than anyone anticipated. Per OPEC latest forecast, we won’t see oil hitting USD60 per barrel until 2020. Only twelve months ago, OPEC forecast for 2020 was USD80 per barrel.

Similar forecasts revisions were produced a month ago by the IMF. In its World Economic Outlook forecast, the IMF revised its outlook for 2016 crude prices from USD50.54 per barrel forecast in October 2015 to USD 42.96 per barrel. 2017 full year price forecast moved from USD55.42 in October 2015 to USD50.64 in October 2016. If in 2015 the IMF was predicting oil prices to hit USD60 marker by mid-2018, today the Fund is projecting oil prices remaining below USD58 per barrel through 2021.

Both, the OPEC and the IMF forecast lower global economic in 2016 and 2017. The IMF outlook is based on world GDP expanding by just 3.08 percent in 2016 and 3.4 percent in 2017, well below post-Crisis average of 3.85 percent and pre-crisis average of 4.94 percent. OPEC forecast for oil prices is based on similarly pessimistic growth outlook for 3.4 percent average growth over the next six years, down from 3.6 percent forecast issued in October 2015.

Alternative Energy: Rising Substitutes

As demand for energy in general remains weak, alternative sources of energy are starting to take a larger bite out of the total energy consumption. Solar power capacity has almost tripled in the U.S. over the last 3 years. Renewables share of the U.S. power supply rose from around 4 percent of total power generation in 2013 to 8 percent this year, on its way to exceed 9 percent in 2017. Solar energy supply is now growing at a rate of almost 40 per annum, spurred on by the Federal solar tax credits, extended by the Congress in early 2016. In Germany, following the Government adoption of Energiewende policies — a strategy that aims to move energy supply away from oil and uranium — renewables now provide almost 30 percent of electricity, on average. And Gwermany’s upper chamber of parliament, the Bundesrat, has passed a resolution calling on the EU to create a system of harmonised taxation and vehicle duties that can ensure that only emission-free cars will be registered in Europe by 2030. On the other side of the spectrum, in the OPEC member states and Russia, renewables energy production is currently standing at below 5 percent of total energy demand. While the number is relatively low, it is rising fast and countries from Saudi Arabia to United Arab Emirates to Russia - all have significant ambitions in terms of lifting non-oil based energy output. In Abu-Dhabi, a recently approved solar energy project will deliver electricity at a cost below coal-fired power plants, at 2.42 US cents per kilowatt-hour, setting world record for the cheapest solar energy supply. Dubai plans to get 25 percent of its energy needs from renewables by 2030. The target is to reach 75 percent by 2050. Even Iran is opening up to use of renewables, with wind and solar investments in 2016-2017 pipeline amounting to close to USD12 billion. In Jordan, just one wind farm - a 38-turbine strong Tafila - is supplying 3 percent of country electricity, since production began in 2015.

All-in, globally, estimated 7 percent of oil demand decline over the last 5 years is accounted for by energy sources substitution. The key drivers for this trend are new environmental agreements, putting more emphasis on alternative energy generation, local environmental pressures (especially in China), and the desire to shift oil production to export markets, away from domestic consumption. Another incentive is to use clean power to reduce domestic subsidies to fossil fuels. According to the IMF report published earlier this year, Middle East, North Africa and Central Asia account for almost one half of the total worldwide energy subsidies. Since the onset of the oil price shock, UAE, Egypt, Oman and Saudi Arabia have been cutting back on fossil fuels subsidies and bringing retail prices for energy closer to market standards.

The second order effect of the above changes in energy composition mix is that moving away from subsidised fossil fuels improves markets transparency and reduces corruption. It also compensates for declines in oil prices in terms of exports earnings.

Drilling at These Prices?

As slower global growth and increasing substitution away from fossil fuels are suppressing demand for oil, supply of the ‘black gold’ is showing no signs of abating. Per latest OPEC statement, oil producers, especially in North America, surprised markets analysts by failing to curb production volumes in response to weak prices. OPEC members have been running production volumes near historical records through out the 3Q 2016. And in the U.S., the Energy Department raised its production forecasts for both 2016 and 2017. However, U.S. crude output this year is unlikely to match the 2015 levels - the highest on record since 1972. All in, the Energy Department now estimates that 2016 average daily production will be around 8.8 million barrel per day (bpd), which is lower than 9.5 million bpd delivered in 2015, but more than forecast for 2016 back in September. Likewise, for 2017, the Energy Department revised its September forecast from 8.57 million bpd to just over 8.7 million bpd in October. Through the second and third quarters of 2016, North American drillers actually increased drilling activity as prices improved relative to late 2015. The number of active oil rigs operating in the U.S. is now up by more than 130 compared to May counts and the rate of new rigs additions is remaining high, rising to 2 percent last week alone.

Russia and Iran

A combination of stagnant or even declining demand, and expanding production means that the only change in the flat trend in oil prices over the next 6-12 months can come only from a policy shock on the supply side. For OPEC, Iran and Russia such a shock is unlikely to happen. Majority of oil exporting economies have either fully (as in the case of Russia and Iran) or partially (as in the case of Saudi Arabia) adjusted their economic policy frameworks to reflect low price of energy environment.

I asked, recently, Konstantin Bochkarev of Forex-BKS, who is one of the leading financial markets analysts working in the Russian markets for a comment on the current state of play in Russian economic policies in relation to oil prices. In his view, “It looks like the worst is over for the Russian economy in terms of adaptations to low oil prices, Western sanctions, geopolitical risks and other challenges of last two years. Sub-50-55 USD oil or even $40 is the new reality and it doesn’t scare any more. On the other hand low efficiency of the economic policy in Russia (due to a lot of constraints like the lack of reforms and the will to change anything before the President election in 2018) means that there’s rather huge cap for the Russian GDP growth which can be limited by 1%-1.5% at 40-55 USD oil.” Overall, “the «crisis policy» which was rather successful during this recession and led to the stabilization of the macroeconomic situations. The recapitalization of the Russian banking system, free float of the Russian ruble, higher interest rates, the transparency of the CBR policy and rather tight budget policy. All these measures finally led to 6% inflation by the end of 2016, rather sufficient decrease in volatility of the Russian ruble and less correlation with oil prices.” And moving away from the petroleum-dominated economy has had even deeper impact. Per Bochkarev, “Oil can’t solve all your problems any more whether it’s 40$ or 100$, because changing social and business environment, external and internal challenges demand something more than budget without deficit or stable cash flow. Still low oil prices can accelerate changes in the Russian economy and society and lead to some necessary reforms or unpopular measures.”

In a sense, Russian experience shows the direction that many oil exporting economies are heading in the age of low oil prices: the direction of accelerated fiscal and monetary responses and gradual structural economic reforms. In some areas, Russia took its medicine first and in a larger dose, but other big producers, including Iran and Saudi Arabia, as well as UAE are also traveling down the same path.

As an aside, it is worth noting that Iranian production is growing ahead of expectations. Per Bloomberg report: “Output at the fields west of the Karoun River, near Iran’s border with Iraq, rose to about 250,000 barrels per day from 65,000 barrels in 2013, the Oil Ministry’s news service Shana reported Sunday, citing President Hassan Rouhani at a ceremony to formally open the project. Iran had expected to reach that output target by the end of the year, Mohsen Ghamsari, director for international affairs at the National Iranian Oil Co., said in September.” (http://www.bloomberg.com/news/articles/2016-11-13/iran-pumps-more-oil-as-saudi-minister-calls-for-opec-output-cuts)

Since the easing of the sanctions, starting with end of January 2016, Iran’s output rose from just around 2.82 million bpd to ca 3.65 million bpd.

Russian producers are also hardly feeling a pinch. According to Bochkarev, “Tax system plays a much more important role in the Russian oil companies production decisions than the rise or fall in oil prices. Whether oil is $40 or $100 per barrel majors are generating generally the same financial results. Besides almost oil majors are stable even at $30 oil. The decreases in oil prices are easily compensated by the fall in the ruble exchange rate. So cost control or cost cutting plays much more important role in other sectors of the Russian economy.”

Still, Russia and Iran might be heading into a direct competition in the European markets, where geopolitics and legacy contracts are changing the playing field away from simple price competition. This new - since January 2016 - competitive dynamic may be a longer term, rather than a current issue, however, according to Bochkarev. “It doesn’t look like that Iranian oil is huge challenge for Russian majors next several years. Numerous consumers who stopped buying the oil from Iran due to sanctions made some changes to their refinery or productions lines and equipment. So Iran has to offer some kind of bonus or lower oil prices to make them return to its oil. Probably it’s much easier for Iran to deal with China, India and other countries in Asia in order to find export markets for its oil. Iran can try to restore market share in Europe but the other hand of such policy can be lower oil prices or necessary discounts. LNG Imports from the US as well as the bigger role of Qatar and Iran in the future are already evident in European markets. The unique status of Gazprom is probably now a matter of the past but the more competitive market can finally make Gazprom more competitive.”

Trump Cards

Which means that economic policies shocks that can alter the current flat growth trend for oil prices are unlikely to come from the OPEC+ countries. Instead, the key to the near-term future variation in oil price trend will most likely come from the U.S. The markets are still assessing the full impact of Mr. Trump’s victory on his foreign and energy policies - the two key areas that are likely to alter the supply side of oil equation, as well as his economic policies that might influence the demand side and inflation. Starting with the latter, if - as promised during the election - the new White House Administration deploys a significant infrastructure and spending stimulus across the U.S. economy, we can expect both the demand for oil to firm up, clearing out some, but not all of the excess supply currently available in the markets. A stimulus to the U.S. growth is also likely to trigger higher inflation. With oil generally being a historical hedge against inflationary pressures, the likely outcome of improved growth performance across the U.S. will be a rise in oil prices from the current range of mid-40s to mid-50s and upper-50s, slightly above the IMF forecasts for 2017 and well ahead of the current market prices.

On the other hand, President-elect has promised to shift Federal supports away from alternative energy toward ‘clean coal’, oil and gas sectors. If he gets his way, the impact will be more American oil flowing to exports and higher excess supply, with lower prices. Mr. Trump’s election is likely to see the Republicans-controlled Congress moving to approve more export-driven pipelines, reducing the cost of oil transport from shale oil rich regions, such as Ohio and Pennsylvania, as well as North Dakota, and increasing incentives to boost production levels. Beyond stimulating production of the U.S. oil, Trump Administration is also likely to green light Keystone XL pipeline that will connect Canadian oil sands to exports terminals in the Gulf of Mexico. This will further expand supply of cheaper oil in the global markets.

Combining the two factors, it appears that the current IMF and OPEC outlook for 2017 for oil prices may be rather optimistic.

Barring a significant surge in global (as opposed to the U.S. alone) growth, and absent supportive cuts to production by the OPEC and other major producing countries, in all likelihood we will see oil prices drifting toward USD52-55 per barrel range toward the second half of 2017. Until then, any significant repricing of oil from USD47-48 per barrel price levels up will be a speculative bet on strong economic growth uptick in the U.S.